Xometry

Made for this moment: The Leading Global AI-Powered Manufacturing Marketplace

This write-up is shorter than my usual analyses as I'm simultaneously preparing another detailed article, but I wanted to promptly share this timely update after Xometry’s quarterly results confirmed the thesis and highlighted the stock’s potential upside.

Disclaimer: This writeup is not investment advice and should not be construed as such. I am sharing my research insights and positioning on individual companies for informational and entertainment purposes. In particular, I do not take into account any readers personal financial situation. Please do your own research.

Business Model

Xometry (XMTR) operates an AI-driven, asset-light marketplace connecting companies that need custom manufactured parts with a global network of qualified manufacturers. Xometry solves the persistent challenges of sourcing high-quality custom parts quickly and efficiently, significantly simplifying procurement and supply chain management for its customers. Buyers get instant quotes on parts, while suppliers benefit from incremental orders and efficient capacity utilization. This unique model positions Xometry to thrive amid ongoing global supply chain disruptions, tariffs, and the broader reshoring trend.

Xometry generates revenue primarily by capturing a spread between the price it charges customers and the cost paid to manufacturers. This marketplace model allows it to earn margins without owning any manufacturing assets, leveraging instead its AI-powered platform to dynamically match supply and demand.

For an overview of Xometry’s unique marketplace model, check out the company's video below:

Q1 Earnings Signal Acceleration(!)

Today’s Q1 earnings release confirms precisely why Xometry is perfectly tailored for the current environment:

Marketplace revenue surged 27% year-over-year, a 700 basis points acceleration from 20% in Q4, driven by strong execution and growth with larger accounts as Xometry continues to capture market share. This pushes total revenue to $151 million for Q1 alone, and $574 million on a last twelve-month basis. Critically, Xometry achieved positive adjusted EBITDA ($0.1 million) for the first time, swinging from a loss of $7.4 million in the prior year. Active buyers jumped 22% YoY, surpassing 71,000, underscoring the platform’s growing indispensability. In my experience, companies reaching such inflection points can provide a strong setup for future returns IF the price paid today is right (more on that later).

CEO Randy Altschuler explained in today's earnings call why the Xometry marketplace is uniquely positioned for the current environment:

"The current volatile and complex international trade and supply chain environment further validates our marketplace model. In addition, there is renewed recognition of the importance of maintaining strong domestic manufacturing bases, which is consistent with our approach."

He also highlighted the power of Xometry’s adaptable model during disruption:

"We navigated this situation before. During COVID, global supply chains were severed, local ones were upended. With our marketplace versus an asset-based approach, we respond to our customers' needs in real time."

Newly appointed President Sanjeev Sahni offered further insights on the strength of their model:

"At Xometry, our supplier network is not tied to dependency on just two or three sourcing markets. This is a real strength: a vast U.S. supplier network balanced by a broad international presence in 50 additional countries."

This slide below from the earnings presentation today illustrates the strenghts of the business model for the current environment:

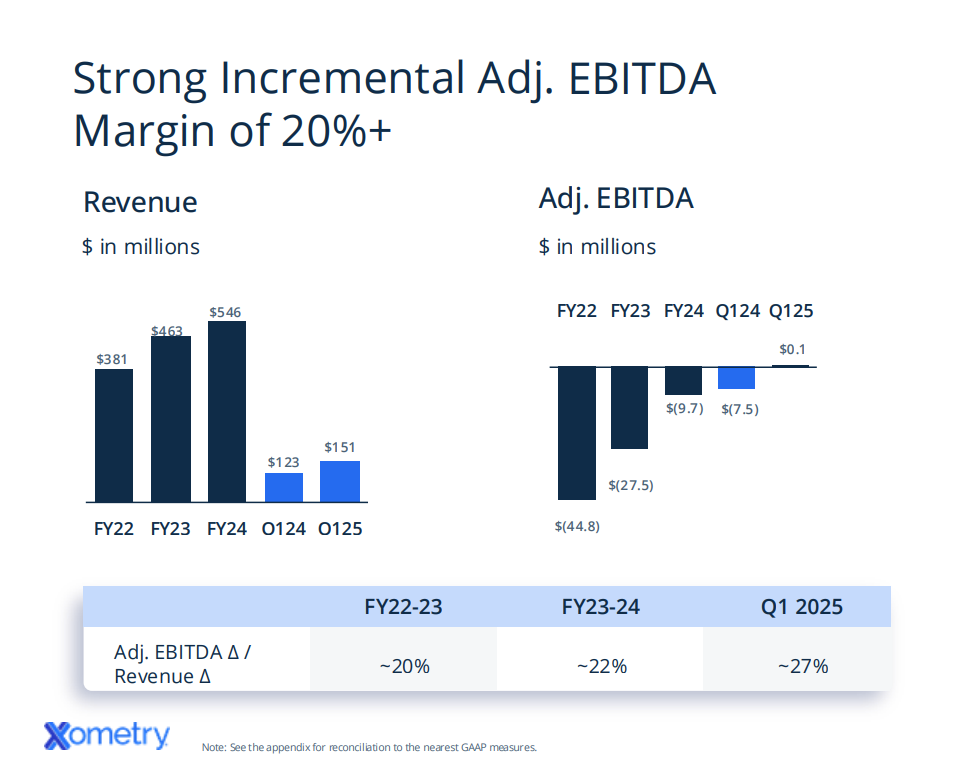

Scaling Into Profitability

Looking forward, financial leverage is clearly kicking in. Xometry has consistently demonstrated operating leverage across the business and switching to EBITDA profitability is only the beginning when the grow north of 20%:

In fact, incremental adjusted EBITDA margins exceed 20% currently, validating the scalability in Xometry's model. CFO James Miln reinforced:

"We delivered an incremental adjusted EBITDA margin of 27%, higher than our long-term target of at least 20%."

Valuation

Xometry’s marketplace gross margin is consistently expanding, reaching 31.8% in Q1 2025: