Too High for Too Long?

Why I am selling my US Stocks in favor of US Treasuries

Introduction:

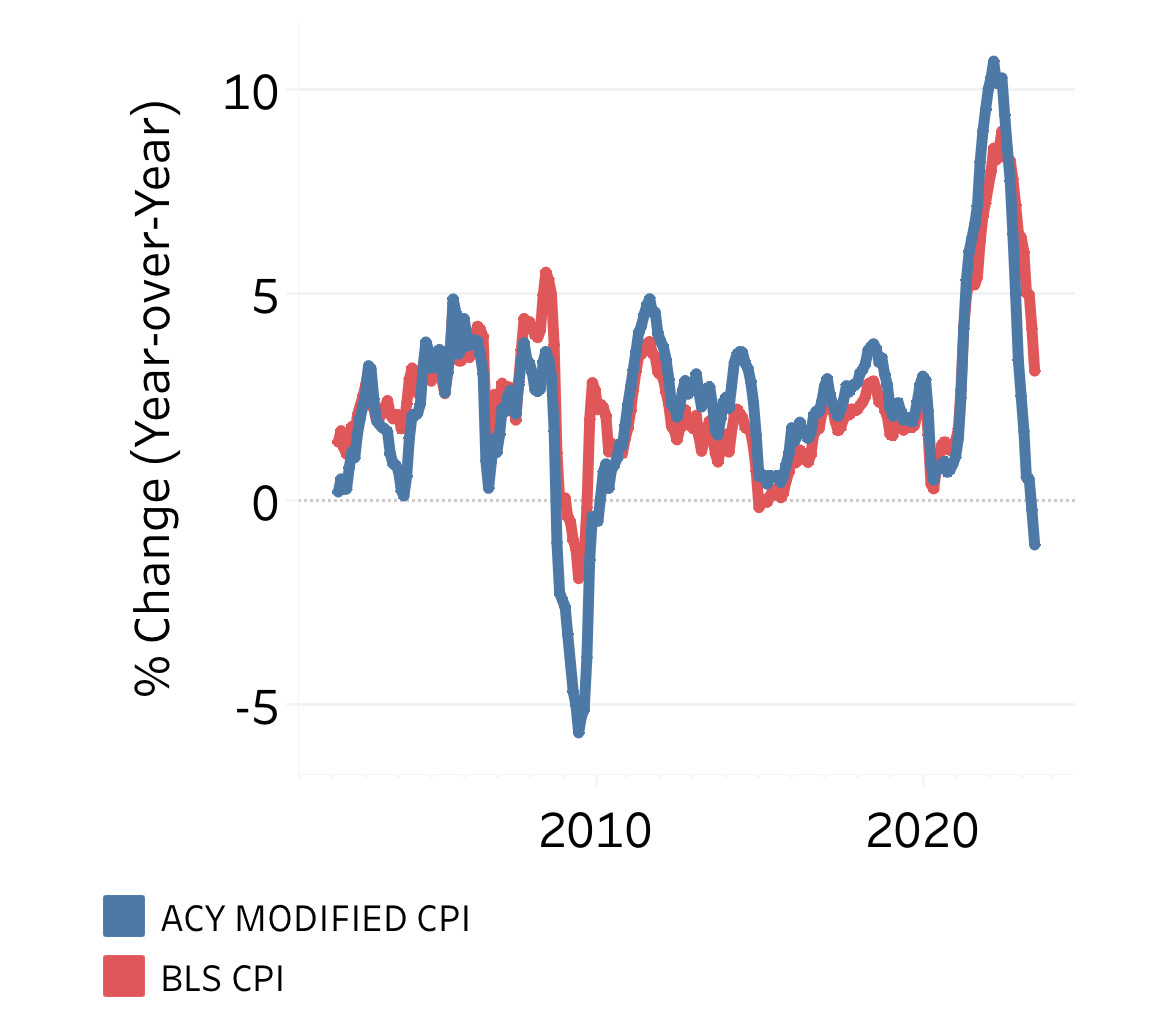

I have always been an optimist about inflation coming down. This conviction has cost me a lot of money in 2022, and it has made me a lot of money in 2023. Despite the notoriously lagged shelter measure that makes up 34% of the CPI, official CPI inflation has come down to 3.0% in the US as of June 2023. The CPI ex-shelter is up only 0.8% since June 2022, undershooting the FED’s inflation target of 2%.

What is the problem with shelter? According to the official CPI statistics, shelter was up 7.8% in June 2023 vs. June 2022. This is obviously nothing more than an utterly lagged measure based on antiquated survey methods. The Case/Shiller home price index shows home prices fell 0.3% between May 2023 and May 2022. More importantly, real time rents also fail to show any signs of inflation. According to Redfin, June 2023 rents were only up 0.5% compared to 12 months ago. Based on Pennstate’s alternative inflation index, marginal rents in June were even down 4.6% year over year. When switching official shelter for actual marginal rents, Pennstate’s ACY modified CPI actually shows -1.14% deflation as of June 2023!

This Rate Hike Cycle is more Brutal than 2008

Meanwhile, the Fed responded to the June inflation rate of 3.0% by hiking rates again to an astounding range of 5.25%-5.50%. The Fed funds rate now matches the peak level of the previous interest rate cycle, which may have contributed to the global financial crisis. However, the current rate hike cycle has been much more aggressive. The 2005 to 2008 cycle started from a base of 1.0%, and rates were raised more gradually over 25 months. In contrast, this time, rates were hiked by a full percentage point more within just 18 months.

Higher for too Long?

Obviously, the economy hasn't faltered yet. Media and experts have grown confident in a soft landing, and the markets seem to reflect this optimism with the S&P 500 up 17% year-to-date (YTD) and the Nasdaq up 33% YTD. However, I'm becoming increasingly skeptical about the prospects of a soft landing, especially since the rate hike cycle appears far from over. The pressing question now is: how long will interest rates remain elevated? While the Fed finished its rate hikes at 5.25% in July 2006, the recession didn't start until December 2008, even though the Fed began rate cuts in August 2007. This historical context illustrates the delayed effects of monetary policy.

Interest rate hikes immediately impact bond prices, which nearly destabilized the US regional banking system this spring. However, it takes longer for these elevated rates to influence the real economy. Most loans are long-term; it's only over time that old, expiring loans get refinanced at steeper rates (or repaid, leading to a contraction in the money supply and a deflationary effect). These higher interest rates now permeate the economy weekly, further straining consumers already grappling with past inflation and loans whose increases haven't kept pace with previous inflation rates. Similarly, businesses now often refinance loans at rates that are double or even triple those of their expiring loans.

The longer this level of interest rates persists, the more profound its impact on the real economy and corporate earnings will be. According to data from Robert Shiller, S&P 500 earnings began to decelerate in 2007 and bottomed out in 2008, i.e., more than two years after the Fed started pausing in July 2006.

As 84% of S&P 500 companies have reported their Q2 2023 numbers, we get a direct glimpse into the economy's state. Data from Factset indicates that revenues have risen just 0.6% compared to Q2 2022. Such a figure isn't consistent with 3.0% inflation and a thriving US economy. Additionally, average earnings have declined by 5.2%, marking the worst outcome since Q3 2020. These real-time statistics present a much grimmer view of the US and global economies, suggesting that the prevailing interest rate level may already be overly restrictive.

The Fed Sees no Interest Rate Cuts in 2023

According to the Federal Reserve's press release on July 26, they may either further raise rates or maintain the current level at the upcoming meeting on September 20:

“In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time.”

FED Presser July 26, 2023

Given that oil prices surged 15.5% in July, I wouldn't be overly surprised if the Fed opts to hike rates again in September. At a minimum, I anticipate rates will remain at their current, notably hawkish level until the November 1st meeting. Powell even mentioned on July 26 that he doesn't foresee the Fed making cuts this year, given his team's lack of expectation for a recession. In an optimistic scenario, the Fed might start trimming rates in small increments by its December 13 meeting. However, my primary expectation is for 25 basis point cuts beginning only on January 30, 2024. If the Fed reduces the rate by 25 basis points at each of the eight meetings in 2024, it would conclude the year with the Fed funds rate still hovering at a notably elevated range of 3.25% to 3.5%. For context, when the global financial crisis-induced recession began in December 2007, the Fed had only trimmed rates from 5.25% to 4.25%. Considering this, I find it increasingly probable that the US may plunge into a recession sometime in 2024, if not sooner.

Why I believe that the FED and the Market are Wrong

The recent Q2 figures from S&P 500 companies clearly illustrate my perspective: I'm skeptical that the US will manage a soft landing given the prevailing interest rates. In my estimation, the window for such a scenario has closed. Interest rates are excessively high, and the timeline for their potential reduction appears prolonged, making a soft landing implausible.

Here's what stands out as problematic:

According to my analysis, the fight against inflation has already been won, but rates remain way too high. This leads to enormous real returns on bonds and cash yielding between 4.2% to 5.3%. The very high cost of debt also encourages paying down expiring loans, rather than refinancing them. This will directly have a negative impact on the money amount, potentially leading to deflation. The following graph shows how drastically the money amount M2 has already fallen relative to nominal GDP.

Regional Banks were already breaking this spring and a larger crisis was only avoided - so far - by the Fed’s BTFP rescue program. However, with the rise in interest rates, unrealized losses on securities have mounted, putting banks that rely on the BTFP program in an even more precarious financial position. This is particularly evident as they lose low-cost deposits in favor of high-interest loans. The looming concern is the credit quality of loan portfolios, especially those tied to real estate. I foresee the regional banking crisis re-emerging as a dominant issue in the next half-year.

Commercial Real Estate is in trouble. US office real estate is suffering from a 18.2% vacancy rate in Q2 according to CBRE data. The resulting drop in operating cash flow combined with substantially increased financing costs will wipe out a lot of equity in US office real estate and some owners will find a strategic default beneficial, passing on losses to the banks, which could further amplify the regional banking crisis. But the dilemma isn't restricted to office spaces. Investment volumes are dwindling — typically a precursor to decreasing prices. Lending is slowing down, indicating one of the tightest lending environments seen in recent times. There's also a surge in vacancy rates in Industrial and Logistics Real Estate. Retail spaces are experiencing dwindling demand, growth in the hotel sector is decelerating, and even the fundamentals of life sciences real estate are showing signs of weakening.

Residential Real Estate, on the other hand, has remained resilient, with the Case/Shiller Index remaining relatively stable year-over-year. However, I'm increasingly uncertain about how long the limited supply can counterbalance the rising challenges in financing new homes. A contributing factor to the current stability is that recent homebuyers are resistant to relocating, fearing the loss of the favorable mortgage rates they secured in the past. With 30-year mortgage rates hovering around 7%, a growing number of homeowners face the daunting task of refinancing at exorbitant rates weekly. At the same time, a substantial amount of new homes supply will come into the market in the next years, which may cause further downward pressure on prices. I anticipate substantial price declines over the next 1-2 years unless interest rates fall way faster than laid out in this article.

The “Student Loan Cliff” - The supreme court has rejected President Biden’s student loan forgiveness plan. Moreover, Biden could no longer extend the student loan moratorium.

Federal student loan repayments will cost an estimated 45 million borrowers around $18 billion per month (Forbes, 2023)

Imagine the situation of 45 million US citizens with a student loan now having to pay on average $400 per month for a total period of three years. At times, there was even reason for hope that part of their debt may have been totally cancelled. This period is so long that its easy to forget about the obligation and adjust the lifestyle accordingly.

"The problem is that if they haven't had to pay a loan for three years, a lot of people don’t have that money in their budget."- VantageScore President and CEO Silvio Tavares

Now these poor borrowers are not only squeezed by inflation and very high interest rates, but from September 1st, they now have to come up with an extra $400 per month (after taxes). I am afraid that this may be the straw that breaks the camel’s back for the US economy.

American Credit Card Debt has reached $1 Trillion.

If, like me, you're wondering how US citizens are affording hotels, flights, and the myriad other goods and services whose prices have skyrocketed, credit card debt may offer some insight. It seems that, even after enduring two years of the Covid pandemic, the consumerist urge remains robust. Initially, the pandemic-induced lockdowns led to a reduction in credit card debt as people remained homebound. However, that trend has now taken a U-turn, which is worrisome. Credit card debt is among the most burdensome due to its high interest rates — a situation exacerbated by the FED's relentless rate hikes. Ideally, US consumers should be hastening to settle this exorbitant debt, but their inability to do so hints at a precarious financial landscape for many.

“The average credit card interest rate in the US as of Aug. 2 was 20.53% – the highest level since 1985, according to Bankrate”

What if the job market turns? Based on points 1-6, it seems the US economy might already be on shaky ground, even though the current US unemployment rate sits at just 3.6%. We've seen this scenario before. Ahead of the Global Financial Crisis (GFC), the US unemployment rate was at a low of 4.4% in May 2007, with the FED funds rate stabilized at 5.25% for nearly a year. Merely two years later, the rate had surged to 9.4%, eventually peaking at 10% in October 2009. My worry stems from the recent aggressive hiring and nominal wage increases. Given the evident weaknesses in corporate revenues and earnings, these might be too aggressive. Instead of renegotiating salaries downward, companies might resort to layoffs. Furthermore, I'm skeptical that the rise of AI will benefit the average worker. It could lead to heightened productivity, which translates to accomplishing more with the same workforce or maintaining output with fewer workers.

In conclusion, I fear that the FED has overtightened its policy and may also be too sluggish in reducing interest rates, risking significant challenges for the US economy.

Equity and Debt Markets: A Disequilibrium

Considering what's been presented, it's clear that the US stock market might have gotten ahead of itself. Meanwhile, bonds have taken a hit, resulting in notably high interest rates.

For context, let’s look at Apple. Before releasing its earnings last Thursday, Apple traded at an expected P/E ratio of 30 based on anticipated 2023 earnings. Although Apple stands as a powerhouse, its current trajectory as a $3 trillion entity suggests it's past its high-growth phase. A significant portion of Apple's earnings growth in the past is due to buybacks. However, topline growth seemed to lose momentum, even before the looming economic challenges. Thus, Apple now has an earnings yield of just 3.3% with limited scope for significant advancement.

Contrast this with the 30-year US treasuries, which are yielding 4.3%, a clear 1.0% advantage over Apple. Plus, these treasuries are risk-free. In comparison, Apple has its own set of challenges, be it competition, aggressive regulatory measures, economic cycles, or the inevitable day when Warren Buffett — its most steadfast supporter — will no longer be around.

With these risks in mind, transitioning from Apple to long-term treasuries appears to be a sound move, especially when viewed through a risk-adjusted lens. Given Apple's substantial impact on the indices, this might just be a broader indication of how stocks, in general, are becoming less appealing than long-term bonds. If, hypothetically, we're heading into a deep recession and Apple's earnings dip by one-third, and its P/E ratio drops to 15, we could see a potential 67% fall in its share price. It may not only be a lost decade for Apple, the share price may never again reach the highs of 2023.

Now, Apple at least has profits. How does the same calculation look for companies without profits or very low profits relative to today’s market cap (e.g. Amazon trading at a next 12 month P/E ratio of 59 while growing ~12%)?

Why I am selling Unprofitable Tech (for Now)