Root, Inc: Disruptive Insurtech Delivers a Turnaround Quarter that Changes Everything

Root, Inc: Disruptive Insurtech Delivers a Turnaround Quarter that Changes Everything

Spoiler: I am Sensing a mid-term 10x and long-term 100x Potential

Summary

Root shocked the market with break even adj. EBITDA and strong growth

Why I think Root has all the ingredients to be a long term success story in a highly attractive industry

Root is now faster growing and vastly more profitable than insurtech peer Lemonade, yet trades at an 85% discount

Disclaimer: This writeup is not investment advice and should not be construed as such. I am sharing my research insights and positioning on individual companies for informational and entertainment purposes. In particular, I do not take into account any readers personal financial situation. Please do your own research.

How Root Differs from Other Car Insurers

To price insurance policies, traditional car insurance companies focus on demographics such as age, ZIP code, occupation, and credit score. In contrast, Root’s business model is centered on providing car insurance based primarily on driving behavior rather than demographics. To get a quote, potential Root customers need to download the root app and drive for about three weeks before they get a quote. During this initial “driving test,” the Root app collects driving data on breaking, speed of turns, times of the day, miles driven, and driving routes. Root doesn’t exclusively price car insurance based on pricing, but the driving test has about a 40% weight in their models.

Root has collected 20 billion miles of mobile telematics data. Their app has been downloaded more than 12 million times. The app also allows drivers to manage their policy and file a claim. Using a proprietary claims system and machine learning, Root allows for automated loss expense, fast claims payout, and thus higher customer satisfaction. Their app has 65,000 reviews with an average rating of 4.7 in the App store.

Root does not insure everyone. While worse drivers will get more expensive insurance policy offers than good drivers, bad drivers may not get a quote at all. These drivers may find a home thought at one of Root’s competitors that don’t emphasize driving behavior the way Root does.

When installing the app, customers give root the permission to “always allow” GPS. A potential concern is that Root customers may be driven in another person’s car. Root claims on their website that their machine learning algorithms identify patterns in location and motion data that are different based on whether one is driving a car vs. being a passenger.

Root does keep monitoring driving behavior after the initial driving test. Root does not routinely use continuous monitoring data for renewal prices. However, they do “react” at times, when folks get much worse over time.

Continuous monitoring is however really helpful on the claims side, when detecting potential insurance fraud:

“You can detect a lot of claims fraud using the mobile device, whether it’s, ‘Hey, you said you were at this location. It doesn’t look like you were,’ so you could push back on some claims, [or] whether it’s, ‘Hey, it looked like you were doing circles. So, we have some suspicion that you were maybe driving for Uber or Lyft. And so it looks like it probably isn’t a personal auto claim. That’s really where we see most of the value of the continuous monitoring versus sort of changing prices dramatically on customers term over term.” Source: CEO Timm in interview with Carrier Management

Root’s “telematics-first” approach using state of the art machine learning methods should allow the company to price policies better than the competition, while also minimizing fraud. This puts Root in a situation where it has all the ingredients to become the cost leader of the industry, while offering the most attractive policies to the best drivers and avoiding those causing accidents.

Moreover, as a company founded only in 2013, Root can build a modern, state-of-the art insurance company, employing state of the art technology and sales channels - an area where legacy insurance companies, often hundreds of years old, may struggle. In particular, incumbent insurers may face the following two structural disadvantages:

Incumbent insurers like Progressive do face certain cost structures that can be different from those of newer, online-based insurers like Lemonade or Root, primarily due to the traditional business model versus the digital-first approach. Here's a detailed breakdown of potential cost disadvantages and advantages:

Broker/Agent Commissions: Traditional insurers often sell their policies through brokers or agents, who receive commissions for their sales. This can increase the cost of acquiring customers compared to direct-to-consumer online models where such intermediary costs are reduced or eliminated.

Operational Overheads: Incumbent insurers typically have more extensive physical infrastructure and legacy systems, leading to higher operational costs. This includes office spaces, legacy IT systems that are expensive to maintain and update, and larger staff for customer service and claims processing.

The Innovator’s Dilemma of Incumbent Insurers

In a Motely Fool interview, Daniel Schreiber, CEO of insurtech peer Lemonade, was asked: What would prevent a State Farm from replicating your business model? I think he put it well, and the incumbent’s disadvantages are an advantage for Lemonade as much as they are for Root.

“Where to begin? We've learned a lot of respect for incumbents like State Farm. I laugh not because they're not tremendous companies with great heritage led by fabulous people, they are all of those things, but because the challenges that they face in the 21st century are incredibly tough, may even be insurmountable in the long term. If you own State Farm or Allstate, any of these companies with state and farm in their name, you have tens of thousands of brokers. You took the job as the CEO thinking that that was a tremendous asset and a defensible barrier to competition, and now you're wondering whether that asset isn't really a liability in the era of direct to consumer digital distribution, and then you've got channel conflict and you can't really go digital and it's holding you back rather that propelling you forward. You were told all these wonderful stories about the technology that you built up since the 1980s, and now you come in and you realize that this is just an albatross around your neck. What you want is a black box, what you've got is a black hole and you keep pouring money into it and nothing really good comes out of it.

You spend decades grooming your team for legacy preservation because you're a 200-year-old company and you thought that the going was good and it would continue that way, and suddenly you're faced with digital disruption and the need for business transformation and you just don't have the culture, you don't have the people. Frankly talking to investors, you don't have the investor base. I've spoken to some CEOs with the largest companies who see the writing on the wall. They say to me these amazing sentences like, "Daniel, I fancy your chances more than fancy my own," which is a stunning thing to hear from some of the largest in terms of the world. When you spend time with them, you understand that even though they know what needs to be done, it would be a huge disruption to their existing business and they won't get support from their shareholders because they have shareholders who don't read The Motley Fool. They've got shareholders who are these large institutions that just want their stable five percent dividend year in year out and will not support strategies that involve transformation. They are hemmed in from their culture, from their technology, from their shareholders. It's the classic innovator's dilemma.”

Root Insurance's innovative approach significantly differentiates it from traditional insurers by leveraging technology to streamline operations and reduce overheads. Their model, centered around a mobile app for everything from policy management to claims processing, inherently reduces the need for extensive physical infrastructure and the large staff complements that are typical of traditional insurance companies. This digital-first strategy not only aims at operational efficiency but also seeks to modernize the insurance experience for customers, potentially leading to cost savings that can be passed on to policyholders.

Telematics at Incumbent Car Insurers

As the benefits to pricing car insurance based on driving behavior are pretty obvious and not extremely difficult to implement, it would be surprising if Root was the only game in town.

Industry leader Progressive is experimenting with telematics since 2013. It currently tries to incentivize customers to opt into Snapshot, its telematics program, by offering a $94 discount for signing up. Moreover, Progressive advertises that customers who renewed their policy, and earned a Snapshot discount, saved an average of $231. Progressive also admits (shown prominently), that the rate may increase with high-risk driving. But, “only” about 2 out of 10 drivers actually get an increase. Many competitors seem to offer similar telematics incentives, so the practice seems to be the current state of the art for incumbents.

However, in sum the industry efforts to lure existing clients into telematics don’t appear to be very successful so far.

A recent study from The National Alliance for Insurance Education and Research and SambaSafety provides some interesting statistics:

27% of commercial auto respondents have internal, dedicated telematics or connected car teams at their organizations

Only 6.25% have robust infrastructures to handle large volumes of telematics data, according to the report.

Approximately 78% of commercial auto insurers are in the research phase of preparing for usage-based insurance (UBI) products.

Another study from “From Perception to Practice: An Insight into Insurer Data Strategies and Sentiments” reports that, “more than half of agents report less than 10% adoption of UBI among their personal auto customers.

It is also very hard to find any credible data on the extent of success that Progressive has with Snapshot. The most recent number I could find was about 8 million clients opting in to Snapshot, which would represent some 30% of Progressive’s clientele. This is respectable, and among incumbents Progressive is probably the technology leader. However, this gives Progressive nowhere near the client pool that Root insurance has. What about the remaining 70%? They probably are not as confident on average about the safety of their driving skills as the 30% that opt in.

Root targets and attracts customers who are comfortable with technology and willing to have their driving monitored closely for the chance to reduce their premiums. This self-selection might lead to a customer base that is, on average, safer. Progressive's broader customer base, even with a significant telematics adoption, may not match this level of self-selection towards safer driving habits.

There is another interesting dynamic at play that relates to the 20% of customers that get offered more expensive policies after the “driving test.” They will likely be personally offended and choose another car insurer, this time not going for their telematics offering. So the bad drivers will be passed around among the incumbent insurers, but they won’t end up at Root, since all new customers have to take the driving test, not just 30% of the clientele.

Root’s Blowout Q4 2023 Quarter

On February 21, Root reported its Q4 results, achieving adjusted EBITDA breakeven for the first time in the company’s history. Even more astonishing, Root achieved this progress in profitability while at the same time achieving strong growth:

Grew policies-in-force 55% to 341,764

Gross premiums written more than doubled to $279 million

Gross premiums earned increased 50% to $214 million

Root’s management attributes much of the progress in this blowout quarter to its technology advantage:

“Our technology advantage demonstrates our ability to effectively match price to risk as evidenced by our superior loss ratios. Our underwriting results improved significantly throughout 2023, with our performance in Q4 2023 marking one of the strongest since our company’s founding. Our gross accident period loss ratio of 66% was produced on record quarterly gross written premium of $279 million. This resulted in a reduction of our Operating Loss to $12 million in the quarter versus $48 million in the same quarter last year. This is strong evidence that our technology advantage continues to evolve and translate into improved unit economics. Further, these results demonstrate our continued, disciplined approach to underwriting by focusing on profitable growth.

At the core of Root’s strategy is our automated data science platform, which leverages proprietary machine learning across all elements of the insurance value chain, including customer onboarding, underwriting, pricing, telematics, and claims. We plan to continue our expansion of these core assets to enhance our connected car capabilities, shorten the algorithm feedback loop, and further automate pricing and claims.

Our technology platform allows us to see changes in claims costs and quickly respond. With this capability, we were able to identify a rapidly changing inflationary environment and adjust our prices to position us for profitable growth. With this backdrop, Root is looking to expand our geographic reach to even more customers.” (2023 Q4 Shareholder letter)

Besides the improvements in pricing and underwriting, Root has shown meaningful progress managing its fixed expense base, setting the foundation for scalable growth:

“As we have achieved our target loss ratio and established a scalable expense base, reaching profitability now largely depends on the level of our discretionary marketing investments. As Root grows, our marketing spend may elevate near-term losses as we do not defer the majority of customer acquisition cost over the life of our customers. Acquisition expenses in our Direct channel will vary, and will be deployed at attractive expected returns over the customer lifecycle.” (2023 Q4 Shareholder letter)

Some further highlights from the earnings call:

On loss ratios: “We are very happy with where our loss ratio is. It is one of the best in the industry at this point.”

On growth: “We are constantly focused on gaining profitable market share. So for us, we don’t think its growth or profit, we are really focused on driving new business at target return levels.”

On pricing: “We are going to continue to improve pricing and underwriting which we believe ultimately will allow us to have a pricing advantage in the market and continue to grow…If there is abatement in the inflationary environment, we think that could certainly be a tailwind to the business.” (CEO Alex Timm)

“…the level of improvement is even more impressive considering the amount of new business that we have achieved….the new business penalty is not huge now. Its single digits right now.”

“…our machine learning underwriting models has really started to improve our segmentation…we’ve been able to bring that first term loss ratio down fairly materially.”

On embedded insurance: “Our ease of doing business, our ability to generate a quote and bid in under a minute is very valuable for customers when they show up on our website or when they show up on our app. Also turns out that’s very valuable for embedded partners when you want to offer insurance to your customers in a seamless experience in as little as 2 or 3 clicks…We do believe we have product differentiation as has been evidenced by the material improvement in attach rates that we have seen on the Carvana platform and we’re going to continue to scale that…we’ve actually added multiple new partners this quarter.”

On profitability: “If we were to stop investing in discretionary marketing spend tomorrow, we believe we would be profitable in the very short term. However we don’t think that’s the right answer for the long term success of the business or for our shareholders.

On customers: “We still target younger folks usually between the ages of 25 and 35 as our primary target audience.

Embedded Channel Marketing

To provide some additional context on embedded insurance - most of Root’s growth comes through the direct channel. Root’s direct channel is driven by “…Our data science driven machine that systematically deploys targeted marketing spend to optimize unit economics and detect trends in the Direct channel also serves as a strong differentiator.”

In addition, Root acquires new customers through the so-called embedded channel. A key example is the Carvana partnership, where Carvana customers can simultaneously buy Root insurance when buying a new used car:

“Through the Carvana work, we basically ‘API-ified’ our entire tech stack, so now it’s very easy and very fast for engineers to effectively plug-and-play with insurance and with the Root technology stack.” (Interview with Carriermanagement.com)

“The Partnership channel is driven by a modern tech stack that can seamlessly integrate into existing platforms, all with a focus on minimal separation between the need for insurance and the purchase of a policy. This includes a wide array of integrations, spanning early-stage marketing partnerships through fully embedded user experiences. We continue to build partnerships across many verticals, including automotive, financial services, affinity, and agency channels. As we grow this channel, we plan to continue to eliminate friction in the purchase experience by moving partners to fully embedded experiences. This allows a seamless purchase experience on the platforms that our customers know and trust.”

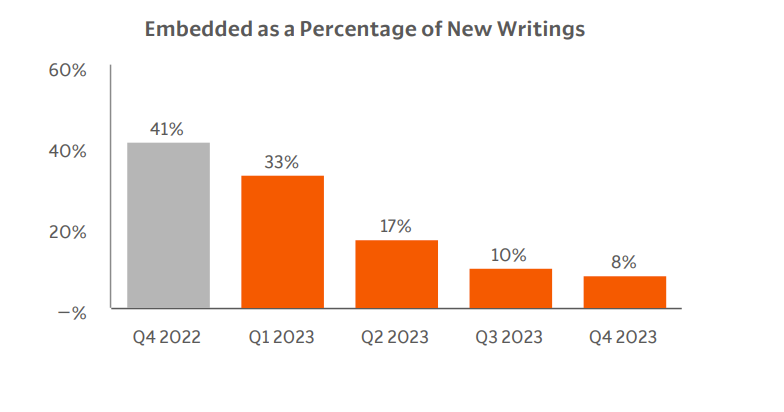

In Q4 2023 some 8% of the growth came through so called embedded channels.

While the embedded channel can be an efficient customer acquisition tool, it is important to note that customers acquired this way do not go through the three week driving test. Arguably, Root will compensate for this disadvantage through a higher initial price for the insurance offer. Moreover, Root can later offer the same incentives as the incumbents to lure these customers into the app.

Valuation

While Root’s share price is up 86% since its stellar Q4 report, the stock is still down 96% from its IPO price:

Root IPO’ed at a $6b market cap in October 2020. Today, the market capitalization is $248 million.

Since Root has just achieved break-even on an adjusted EBITDA basis, traditional valuation metrics such as price-earnings, or price-to-book cannot be applied. Nevertheless, there is a right price for everything. Root insurance is using an innovative approach to take market share in an industry that has seen very little innovation so far. The progress in 2023 has given new life to the high hopes around Root’s IPO. In my opinion there is now again a significant probability that Root is a long term winner in a very lucrative industry.

Comps

Just to illustrate what is at stake in this industry. Car Insurer GEICO is certainly among Warren Buffett’s most iconic investment. Moreover, Progressive has been one of the best performing US stocks of all time, up 683x(!) since IPO in 1984:

As a benchmark, Progressive has 30 million policies in force and trades at a market capitalization of $112b, about 2x its volume of annual gross written premium. This shows that even at scale a mature industry giant can, if well run, trade at a significant premium to its volume of premiums written.

Insurtech peer Lemonade currently has a market cap of $1250m. By the end of Q3 2023, Lemonade had $719m in-force-premium, up 19% year over year (vs. +81% at Root in Q4). Lemonade’s bottom line in Q3 improved to -$40m adj. EBITDA in Q3 or -$160m annualized. Lemonade currently trades at a multiple of 1.74 relative to its in-force-premium. To be clear, I do not think that Lemonade is currently overvalued. While the company has a lot to prove, I think more likely than not, Lemonade will turn out a pretty good investment from current price levels.

Root currently trades at a market capitalization of $248m. Root’s in-force-premium by the end of 2023 Q4 was $973m. Root is not only growing much faster than Lemonade, but Root is also way more profitable, having achieved adj. EBITDA break-even in Q4. If anything, one might expect that Root trades at a significant premium to Lemonade. However, Root trades at only 0.25x in-force-premium vs. 1.75x for Lemonade. Root trades at an 85% discount to Lemonade, when it should arguably trade for a premium.

If Mr. Market is pricing Lemonade correctly, then Mr. Market is currently pricing Root for bankruptcy. Bankruptcy might have been a possibility before Root’s stellar Q4 report, but certainly no more at this point, in my opinion. Root has more than $500m in unencumbered cash and just achieved break-even. Heck, Root’s market cap is a 50% discount to its unencumbered cash position. Frankly, I have no idea what Mr. Market is thinking at this point. To me, it looks like despite the 85% move post earnings, the market has been way too slow to update its opinion about Root.

To some extent this is understandable. The stock long looked like a dumpster fire on the way towards bankruptcy, so why would anyone care. It makes sense a micro cap with $100-150m market cap and bad numbers would be neglected by the market.

However, the Q4 report has changed everything. The Q4 report should in my opinion revive the level of excitement that surrounded Root around its IPO. Three years after its IPO, Root has finally delivered. Back then the market wanted “growth, growth, growth.” CEO Timm and his company had to adapt to a new reality. With the Q4 report, Root has evidently achieved a solid foundation for prudent growth. Who will now stop Root from taking market share with its unique competitive position in a market that seems ripe for another chapter for “The Innovator’s Dilemma”?

I believe the market has only begun to notice the potential. For a stock that is down 96% from IPO, there should be enough shorts out there to lay out the bear case. I am interested in the bull case. There are two ways that Root could be a 10x:

Short term: Root would be a 10x if it traded at a multiple of 2.5x relative to its in-force premium (less profitable and slower-growing insurtech peer Lemonade currently trades at 1.74x).

Mid term: If Root grows its in-force premium by 44%, the same 1.74x multiple of Lemonade would also result in a 10x increase of the share price. At the current pace of growth, I believe that Root should achieve 44% in-force premium growth over a period of 1-2 years.

Over the long term, it is the first time in a while that I sense the potential for a 100-bagger with Root. 100-baggers are rare. A dirt-cheap valuation is a good starting point. As laid out above, my current fair value estimate for Root is about 10x higher than today’s share price. Now, a 100-bagger would take another 10x that has to be driven by fundamentals.

At the end of 2023, Root had 342k policies in force, about 1.14% of Progressive’s 30m policies. With the current strength of Root’s business model and positioning in the market, it does not take a crazy level of imagination that Root can grow policies 10x to 3.4m. At a CAGR of 26%, it would take Root 10 years to get there. Note that even after a 100x, Root’s market cap would be “only” $24.8b, a mere 4x from its IPO valuation in 2020.

Risks

My long-term followers would probably argue that I have an “optimism-bias” relative to most other investors. In fact, I do like to take contrarian positions (and also Root has some 10% short ratio), and usually on the long side. My “bullish” assumption may simply not play out or Root keeps getting ignored by the market. Moreover, while adjusted EBITDA was at break-even, it still takes a bit more to be profitable on a GAAP basis and if the company fails to do so, it will be impossible to achieve the grand slam scenario laid out here. But I think Root has a shot at getting there and I am putting my money where my mouth is with a 5% position in Root. If it was a sure thing, I’d put in 20%, so do with that information what you think.

Besides this general uncertainty around assumptions and how exactly the future plays out, there are two factors that I believe investors in Root should track:

$300m five year term loan

Root has an expensive $300m five-year term loan, issued on January 26, 2022. The maturity is January 27, 2027. The interest rate is determined on a floating rate basis on the SOFR, with a 1% floor, plus 9%, plus 0.26% p.a. In 2023, Root’s interest expense was $46m.

I am not too worried about this loan. At the end of 2023, Root had $171m short and fixed term investments plus $679m in cash. Unencumbered cash is above $500m and Root earned $30m in net investment income.

With the business now operating at break-even, I believe chances are good that Root can refinance the loan at much better conditions in 2027. However, should operating performance deteriorate, the loan might become a concern again, and at the current market capitalization, there is no point in raising equity.

Self-Driving Cars

In the future, self-driving cars might become ubiquitous. IF these self driving cars are ubiquitous, then only because they are much better drivers than humans, so accidents should go down, perhaps dramatically so.

On the other hand, this may never happen. Elon Musk has been promising robotaxis since 2018 at least and 6 years later, we are still not there. Regulatory hurdles will be enormous. There will be setbacks. Its “happens” to die in a self-caused accident, but dying due to the mistake of the robots / algorithm? I don’t think society is ready for that. Even if we have a 100% robotaxi future, how long will it take to get there? Will everyone be able to afford these? When will the last humans be taken off the streets? And until that has happened, there will be accidents.

In sum, a self-driving, accident free future is a possibility, but which investment is really risk free? I guess I am taking my chances at this point.

naccidents strongly decrease