Meta Platforms

Meta Platforms

Expanding Online Real Estate with a Growing Moat

Summary

Meta’s family of apps is a great business with a growing moat and a long growth runway.

Meta should return to significant revenue growth next year, overcoming temporary macro-, IDFA-, and short video challenges.

Long term investors to benefit from multiple expansion: In 10 years, metaverse overhang will be gone either due to success, or Zuckerberg giving up.

Bear case (writing off metaverse): 15% p.a. next 10 years with modest buybacks and revenue growth of just 4% p.a.

Base case (writing off metaverse): 11x over the next 10 years with modest buybacks and revenue growth of 12.5% p.a.

The Opportunity: Meta’s Share Price vs. Fundamentals

Over the last five years, Meta Platforms (formerly Facebook) has grown earnings per share by ~300% from $3.49 in 2016 to $13.77 in 2021. Meta’s revenues have increased 338% from $26.9b in 2016 to $117.9b in 2021. At the same time, the share price is still at $167 - exactly the same as five years ago. As a result of this discrepancy between the development of the fundamentals vs. the share price, Meta today trades at a price-earnings ratio of just 12 based on 2021 earnings per share. Focusing on the core family of apps business and backing out cash, Meta trades at an astonishing 7.2x multiple on its 2021 operating earnings.

In this write-up I will explain why I consider Meta Platforms a great business with a long growth runway and a growing moat. I will discuss how the stock can deliver a shareholder return of 15% p.a. over the next 10 years, even in a bear case scenario without real growth and completely writing off all of Meta’s augmented and virtual reality (AR/VR) investments. I will also lay out why in my base case scenario Meta’s family of apps will return to significant growth over the next decade. If this scenario materializes, an investment in Meta today can be a 11x over the next 10 years (27% p.a.). Importantly, this outcome can be achieved whether or not Meta’s AR/VR investments succeed. For the latter scenario, I expect CEO Mark Zuckerberg will finally give up his metaverse ambitions and instead allocate free cash flow to significantly ramp-up share buybacks.

Today’s share price is depressed in large parts due to investor skepticism about Meta’s AR/VR investments. In 2021, operating losses in Meta’s “Reality Labs” division amounted to $10.2 billion and in the first half of 2022, the losses of this segment are even 36% larger. Zuckerberg is clearly committed to heavily investing into AR/VR for the mid term.

In 10 years, either Mark Zuckerberg or investors will have been proven wrong. If Zuckerberg is right, investors will sit on an even stronger business, where Meta can expand its online real estate empire endlessly in the metaverse, while being independent of Apple’s iOS and Google’s Android smartphone platforms. If metaverse-critical investors are right, I expect Zuckerberg, as a rational owner, will give up his metaverse ambitions within the next 5 to 10 years, freeing up more than $10 billion in free cash flow per year for additional share buybacks. In both scenarios, the overhang that depresses the valuation of Meta today will be gone. As a result, Meta’s terminal valuation should be much closer to a market-level price earnings ratio (today the S&P 500 trades at a P/E ratio of 20.7). This multiple expansion alone is an almost free arbitrage opportunity for long term investors.

Why Meta Platforms is a Great Business

The world of physical real estate is all about “location, location, location.” The residential real estate with the best views, in the safest area of the town, and the best schools around will attract the highest prices by potential home buyers or tenants. Likewise, the city’s prime retail shopping street will attract Luis Vuitton and Apple stores because they attract a steady footfall stream of the most affluent customers. In turn, retail tenants pay up for the right to rent these prime real estate locations.

Today, Facebook and Instagram are no longer mere social networks to connect with family members and friends. They have evolved into personalized magazines where people also shop, follow their interests & hobbies, their favorite musicians and actors, and where they discover new content suggested by Meta’s artificial intelligence (AI) algorithms. In sum, Facebook and Instagram are places most of us go to every day in order to be entertained. Since these places are no longer in the physical world, but online, I view Meta’s family of apps as online real estate, where businesses pay rent to Meta in the form of advertising dollars in exchange for ad space.

Online real estate is superior to physical real estate, because it enables businesses to show their products to potential customers 24/7, i.e. not limited to the regular business hours of the physical world. Moreover, Meta’s treasure trove of data enables its AI to show each user the right ad at the right point in time, to exactly those customers with the highest chance of actually buying the product. In contrast to a high-street retail store, Meta’s would not show a Luis Vuitton product to a customer who could not afford the product. For the user, this has the pleasant advantage that the ads on Meta’s family of apps are typically relevant (=interesting) and thereby far less disruptive to the experience compared to virtually all other online platforms.

Over the last decade, Meta has steadily increased its online real estate empire through the acquisitions of Instagram and WhatsApp, and by massively growing the number of users on its platforms. As of June 30, 2022, Meta has 2.88 billion daily active people (DAP) across its family of apps. This represents 37% of the world population. Most of Meta’s DAP use more than one app on a regular basis, typically at least Facebook and Instagram. Moreover, in most of the Western World ex the US, the usage of WhatsApp is ubiquitous and has effectively replaced all mobile messaging and phone calls in those countries.

Meta’s family of apps represent a formidable online advertising platform for businesses, because they provide access to 2.88 billion DAP, each of them spending a significant amount of time per day across the different apps. In terms of marketing efficiency, Facebook and Instagram provide among the highest return on ad dollars for marketers when compared to other forms of advertising.

Advertising on Meta is complementary to advertising via google search. Google is effectively “pull advertising,” as the customer already vaguely knows what he wants. In contrast, advertising on Facebook & Instagram is “push advertising.” It allows businesses to showcase their products, which the customer does not yet know he may want; trigger desire, win new customers. And nobody’s AI is better suited than Meta’s to provide the best fit between products and potential buyers. Both types of advertising will continue to co-exist, representing the two essential pillars of any reasonable marketing strategy.

In 2021, Meta’s family of apps delivered operating income of $57 billion on $115 billion in revenues, leading to an operating margin of 50% (up from 47% in 2020 and 41% in 2019). Margins are this high, because Meta essentially aggregates content for free and distributes it to individual users, through its ever-improving artificial intelligence algorithms. Costs are modest, because online real estate is built using bits and bytes, rather than bricks and mortar, and rarely requires new “land investments” such as for acquisitions of Instagram and WhatsApp, or most recently laying the foundations of the metaverse with its AR/VR investments. Once the infrastructure is in place, Meta is scaling the platforms and increasing the desirability of spending time in their online space with ever-improving features.

Operation and maintenance of online real estate is inherently scalable. Facebook doesn`t need to pay security guards or buy expensive insurance to protect a Luis Vuitton store. Instead, Meta needs to moderate content, but it does so nowadays does so mostly via scalable AI solutions. The inherent scalability of the business model should lead to even higher operating margins in the future if Meta keeps increasing revenues, or at least defend the current level of 50% operating margins.

Many investors consider Google’s search business the greatest business model in time. True, Google’s search monopoly may be close to impossible to disrupt. For Meta, the consensus seems to assume the opposite. Many investors point to hypothetical negative network effects: Should some users start to leave for another platform, the utility of the remaining users also goes down in theory, potentially leading to a fast collapse of the social network.

This take may have been correct for a year 2005-style pure friends network like MySpace. It misses what Facebook and Instagram represent today: the “friends” part is still significant, but just one aspect of the bigger picture: Consider a user who goes to Facebook to buy and sell on its marketplace, follow his niche interests in Facebook groups, and is entertained reading the news and watching some short form videos. Such a user’s utility from visiting Facebook will diminish marginally at worst, even if 30% of his family and friends should suddenly leave. Inverting this idea, another competing social network would have to be able to onboard new users, replacing the Facebook utility, while still providing a smooth technical experience - its close to impossible to achieve that in a short period of time. It is exactly that window of opportunity, which allows Meta to adapt any new desirable social network feature and use its distribution power to roll it out to its much larger user base.

In sum, Meta’s moat is already substantial and in the following section I will describe why I expect its moat to further increase for the years to come.

Growing the Moat: Social Network Evolution and Meta’s Power of Distribution

Meta’s critics emphasize a perceived fragility of social networks, pointing to the rise and fall of MySpace over 15 years ago. I have a different view: competition stimulates better business. This can be a welcome feature IF you are the top dog with distribution power. Meta has demonstrated over and over again that it can adapt desirable features from other platforms, often further improve them, and then roll out these new features to their much larger user base compared to that of the emerging competition, thereby strengthening the moat of its own platform as it becomes ever less likely to kick the top dog off its throne.

I am convinced that Facebook and Instagram would represent much worse experiences today had they never been challenged by competitors. In this alternative universe, Facebook and Instagram would represent a larger piece of a much smaller cake. Here are a few examples how Facebook and Instagram’s competitors helped them build more desirable online real estate:

2012: Facebook launches “follow” feature to consume content from non-friends (Twitter had implemented followers from day one)

2013: Facebook launches “verified profiles and pages” (Twitter launched verified accounts in 2009)

2016: Instagram launches Instagram “Stories” (Snapchat introduced “Stories” in 2013).

2021: Instagram and Facebook launch the short form video format “Reels” (a signature feature of short form video platform TikTok).

This is adaptive evolution, which benefits the incumbent that can adapt and not only survive, but strive if it only manages to stay the fittest.

Without doubt, Facebook has experienced the rise of multiple competing social networks, nullifying any credible monopoly accusations. Nevertheless, it can be argued that thanks to Meta’s strong execution in adapting key features of their competitors, it has ensured to keep them at bay, limiting them to rather niche specialists in comparison to the breadth and scope of Facebook and Instagram. For example, Instagram’s stories feature is today used by a way larger part of humanity than Snapchat’s stories, where usage is effectively limited to teens and young adults (most of whom are also using stories on Instagram).

The current case of TikTok is considered an existential threat for Meta by many investors. At the same time, the TikTok case highlights the opportunity for Meta. In this moment, billions of Facebook and Instagram users are getting introduced to entertaining short form videos (Reels), while they have never downloaded TikTok. Admittedly, TikTok is certainly the most formidable competing “social network” today. Meta should have responded to the threat way earlier. On the other hand, it also seems to me that TikTok largely misses the “social” aspect, as user activity is basically limited to the passive consumption of videos.

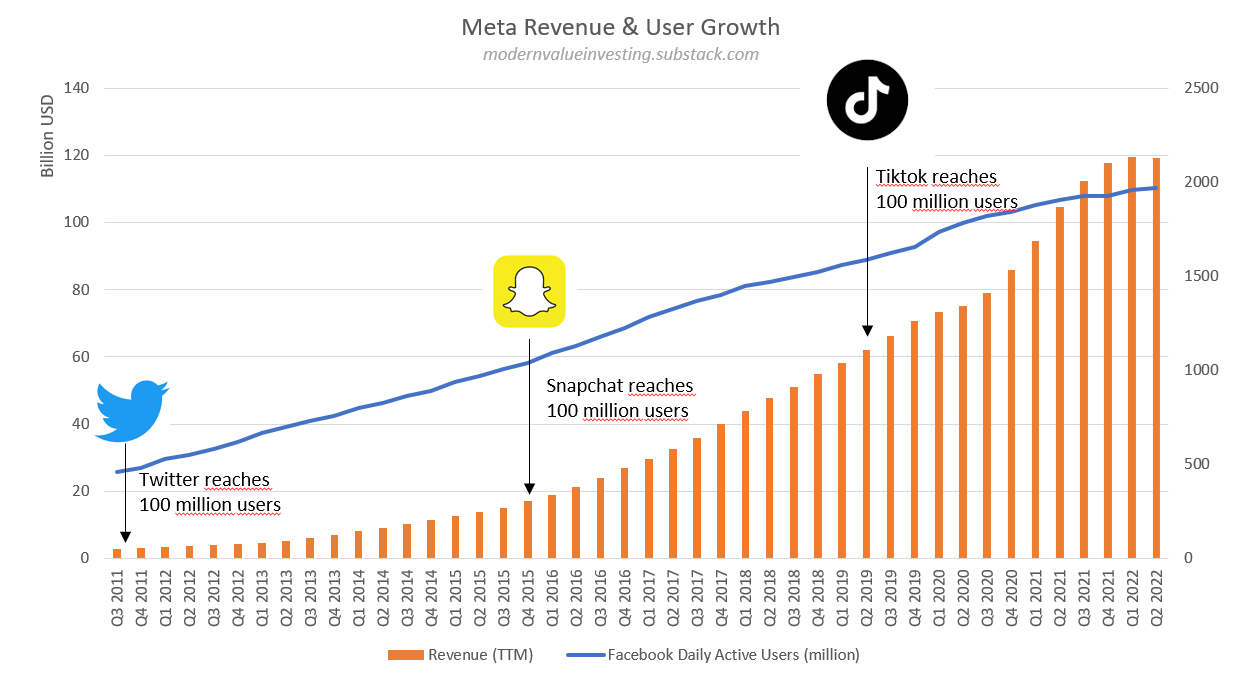

But aren`t Meta’s competitors grabbing significant mindshare? Sure they do, but maybe more importantly, they have contributed to growing the pie. Lets have a look at some hard data as a factual basis to evaluate whether or not emerging social media platforms have negatively impacted Meta. The following graph illustrates Meta’s revenue growth as well as the number of daily active users for Facebook’s blue app. In addition, the graph shows the point in time at which emerging competitors have reached 100 million users.

Obviously, none of today’s globally relevant social networks was able to stop Meta’s track record of revenue and user growth. If anything, the opposite seems to be the case. This may be a less surprising insight in light of my discussion of Meta’s adaptive evolution above. In contrast, Meta’s online real estate appears to become significantly more valuable following the adoption of new key features of its competitors.

A final evaluation regarding the impact of the adoption of Reels is still outstanding. However, in the recent earnings call, management already revealed that Reels are additive to time spend:

“Reels engagement is also growing quickly. I shared last quarter that Reels already made up 20% of the time that people spend on Instagram. This quarter we saw a more than 30% increase in the time that people spent engaging with Reels across Facebook and Instagram. AI advances are driving a lot of these improvements, and one example is that after launching a new large AI model for recommendations, we saw a 15% increase in watch time in the Reels video player on Facebook alone. So I think that there are many improvements like this that we'll continue to make.”

Mark Zuckerberg on the 2022 Q2 earnings call

The Q2 call also revealed that Reels allowed Meta to increase the number of ads shown to its users by 15% year over year. The full impact on monetization will be seen over the coming years. As a reminder, the push to “Stories” also took a number of quarters to reveal the full benefits in terms of monetization.

Is Facebook Still Relevant?

Facebook’s blue app is often considered “dead” by many investors, they claim nobody uses it anymore, probably inferring from their personal habits to the rest of the world. They couldn`t be more wrong. While Facebook is not alone anymore, it is stronger than ever with 2 billion daily active users across the globe (still rising), each of them spending on average about 30 minutes per day on the app. To understand the ongoing rise of the blue app, one must understand the increased depth of the services offered by Facebook. Here are a few current statistics that stood out to me (see more up to date key figures in this link):

Over 1 billion stories get posted every day across Facebook, Instagram and WhatsApp

Facebook is the favorite social platform of the 35-44 demographic

57% of Americans say Stories make them feel like part of a community

31% of Americans regularly get their news from Facebook

1.8 billion people use Facebook Groups every month

Facebook Marketplace has 1 billion monthly active users

There are 250 million Facebook Shops worldwide

Facebook beats out TikTok for short-form video with 60.8% of user share

Facebook gaming overtook youtube gaming in Q3 2021 with now 15.7% market share (gradually catching up to Twitch (80.5%)

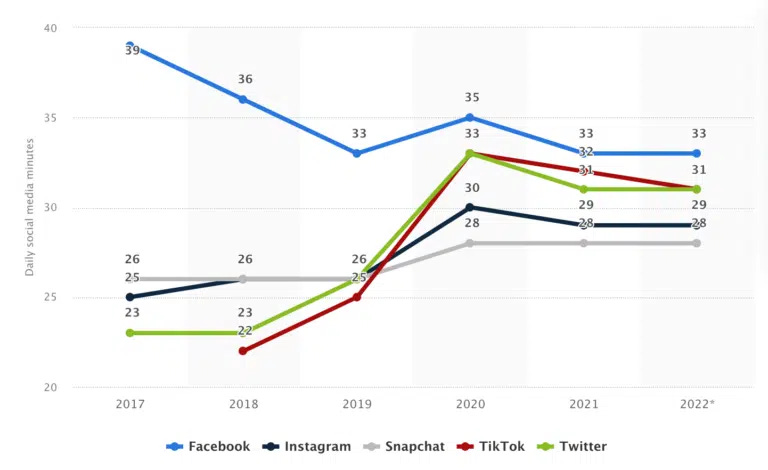

Users spend an average of 19.6 hours a month on Facebook, or 33 minutes a day (Source: Statista). Note also in the following graph how TikTok usage seems to have peaked.

Revenue Growth

Over the last five years, Meta has grown revenues at an annual growth rate of 34%. To understand the drivers of Meta’s revenue growth, consider the following formula:

Revenue = f(Number of users; time spent per users; ad load; price per ad)

The size of Meta’s family of apps online real estate empire can be expressed by the number of ads it can show to its users. The number of ads itself depends on the number of users across all of Meta’s platforms, multiplied by the amount of time each user spends on the platform, and of course the ad load, which is the number of ads Meta shows to its users over a given time period.

It is evident that Meta is still growing users with the reliability of a Swiss watch. This even holds for its most mature platform, the blue Facebook app. Instagram and WhatsApp are still showing strong user growth. Even in the U.S. where Apple’s iMessage system is dominant unlike in the rest of the world, WhatsApp is now regularly in the top 10 of the iOS app download charts.

The amount of time each user spends on the platform is currently increasing because of the successful rollout of Reels, but also initiatives like the Facebook Marketplace or Groups get users to spend more time inside Meta’s online real estate.

Ad load on Facebook and Instagram could be thought of as rather mature until the recent rollout of Reels. As users spend more time watching Reels (with currently very modest ad load), Meta will sequentially increase the ad load to an optimal level. Further growth runway for ad load clearly exists on its WhatsApp platform which is effectively still unmonetized and ad free to date.

The probably largest lever for Meta to keep increasing revenue is via the price per ad. Return on marketing dollars for advertisers is still exceptional on Facebook and Instagram compared to most other forms of advertising. In an efficient advertising market, there should be no free lunch and the return on advertising should hence be similar across all platforms. I expect this factor alone to provide plenty of revenue growth runway for Meta.

As if that’s not everything, Meta is steadily improving the quality of ads shown to its users by providing advertisers with the respective tools. Over time, advertisers learn to use advertising on Meta’s platforms in the most efficient way. Long term, the effectiveness of ads in the metaverse could leave picture or video ads in the dust.

Finally, Meta is exposed to significant long term tailwinds. Online advertising is still expected to strongly expand over the next decade. Even at maturity, online advertising is essentially a tax on the strength of the economy. Hence, Meta’s revenues at scale should grow not only with the inflation rate, but also real GDP growth. In this regard, I am excited about Meta’s exposure to South East Asia and India, regions where GDP will grow at high rates for decades to come. To give you a sense of the opportunity: In Q2 2022, Meta’s average revenue per Facebook user was $53.01 in the US, but a mere $4.16 in Asia-Pacific. I expect Meta to keep increasing revenue per US users, but should revenue per user in Asia-Pacific one day reach today’s level in the US, that factor alone represents a 1174% revenue growth opportunity for the Asia-Pacific region.

In summary, the long term outlook for revenue growth is very solid, even without touching the opportunity of the metaverse. Pre-covid, Meta was growing revenues at more than 20% p.a. I expect Meta’s normalized revenue growth rate to be currently in the 15% to 20% range. In the first half of 2022, revenue growth of the family of apps segment was however only 2.1%, or ~5% on a constant-currency basis. I estimate current revenue growth is muted because of the following short term impacts:

Apple’s IDFA / privacy changes have limited Meta’s tracking capabilities. This reduces its targeting efficiency, as well as capabilities to attribute ad conversions. The CEO estimates the impact is circa $10 billion per year. For the 2022 financial year, I therefore expect that Apple’s IDFA changes will reduce Meta’s revenues by ~8% ($10 billion relative to $117 billion family of apps revenue in 2021). I consider this a one off reset, and expect continued revenue growth in 2023 from that lower level. As an additional optionality, Meta is working hard to improve targeting capabilities and attributions and may regain some lost ground.

Macro turbulences. High inflation has forced central banks across the world to raise interest rates at unprecedented levels. Shockwaves have gone through the economy in Q1 and especially Q2 and will most likely last for a while. This affected all advertising platforms as evidenced by Q2 earnings reports. Next year, however, we will hopefully see an improvement of the macro situation. Moreover, Meta will then have rather easy to beat 2022 comps. For the 2022 financial year I expect the macro turbulences to reduce Meta’s revenues by ~5%.

Cannibalization from Reels. Finally, Meta is aggressively rolling out Reels. This has led to 15% growth in the number of ads, at the same time the average price per ad is down 15% (partly due to IDFA and Macro). It takes time for advertisers to adapt the new format, moreover Meta is actively steering user attention away from established formats with high prices per ad. We have seen how this played out with the rollout of stories in Instagram and Facebook. Reels will be no different. I expect the cannibalization from Reels has a ~5% impact on 2022 revenues.

I expect circa 2% revenue growth for Meta’s family of apps business in 2022 (in line with H1). Without the effects from the rising US dollar, IDFA, macro, and cannibalization from Reels, Meta might have achieved ~23% revenue growth by my estimates.

While the current reality is what it is, I consider 23% a better baseline for Meta’s current revenue growth power than the 2% we will see for this year. Going forward, I am expecting 18% revenue growth for 2023 in my base case scenario. Given the outlined long term tailwinds of Meta’s business model, I do not expect fast revenue deceleration. For my long term base case model, I expect Meta will grow family of apps revenue from $118 billion in 2022 to $385 billion in 2032, which represents a 12.5% revenue CAGR. In this projection, revenues will still grow 8% in 2032, suggesting that Meta is fundamentally still a growth stock relative to the market average, hence deserving higher multiple than a market average P/E ratio of 20.

A Bear Case with 15% Return per Year?

As an investor, I aim to achieve a return of at least 15% per year. This roughly equates a doubling of the investment value over five years, or a 4x over 10 years. What does it take for Meta to provide a shareholder return of 15% p.a. over the next decade? Spoiler: Not much!

For my bear case scenario I assume that Zuckerberg’s metaverse investments are a total failure, creating zero value, effectively burning some $10-15 billion over the next 10 years in return for nothing. I think this assumption could not be more conservative (if not straight unrealistic). Moreover, I ignore Meta’s current cash pile of $40 billion in this valuation.

Essentially, any value in my bear case scenario is derived from the terminal value of the family of apps segment by 2032 and the share buybacks in between. Zuckerberg is committed to the share buybacks. Between Q2 2021 and Q2 2022, the total number of diluted shares outstanding was reduced by 5.7%. For my bear case scenario, I assume Meta buys back 2.5% of shares per year (after compensating for stock based comp). Accordingly, Meta’s share count would be just 77.6% in 2032 relative to today’s share count. At the current market cap, buying back 2.5% of shares requires just $11.3 billion. However, I expect the share price to recover, thus requiring more than $11.3 billion per year in the future to buy back the same 2.5% of shares per year. If Meta’s share price doubles, 2.5% buybacks could be maintained with $22.6 billion per year. Meta’s free cash flow in 2021 was $38.4 billion, leaving enough room for significant share buybacks while also investing >$10 billion p.a. into the metaverse.

For Meta to be a 4x over 10 years on a per share basis, its market capitalization only needs to grow 3.1x due to the effect of buybacks (4.0 x 77.6% = 3.1). Today’s market cap is $451 billion, so Meta’s market cap would have to grow to $1398 billion. I also assume that at the latest after 10 years Mark Zuckerberg would give up his metaverse ambitions. As a consequence, I assume the metaverse overhang depressing the share price today will be gone and I model Meta trades at a P/E ratio of 20 at the end of 2032. This means Meta needs to achieve earnings of $69.9 billion per year from its family of apps business by 2032. Operating earnings from the family of apps segment were already $56.9 billion in 2021. Assuming an effective tax rate of 20% (17% in 2021), the hypothetical earnings from the family of apps business was $45.5 billion in 2021. This means earnings from Meta’s family of apps would have to grow 53% from 2021 to 2032, or 4.0% per year, which is little more than current inflation expectations.

In sum, Meta’s family of apps needs to grow at little more than the inflation rate for the next 10 years in order to achieve a shareholder return of 15% p.a., despite wasting more than $100 billion in total on the metaverse in return for nothing.

Base Case: 11x over 10 years

As outlined in the revenue growth section, I expect Meta to grow revenues in its family of apps business from $118 billion in 2022 to $385 billion in 2032, representing a 12.5% revenue CAGR. Moreover, I expect 8% revenue growth in 2032, the final year of the projection period. This suggests still above market-average growth for a number of years to come, hence Meta would be deserving an exit P/E multiple of 25 vs. a market average P/E ratio of more or less 20 today for the S&P 500.

A P/E ratio of 25 in 2032 may seem high, when today the stock actually trades at basically just half that multiple. I argue that today’s valuation overhang from the metaverse uncertainty will be gone by 2032. Either the metaverse is a success and Zuckerberg will keep investing, but now with the full support of shareholders, or he will give up by then. Moreover, I believe that by then 25 years after the fall of MySpace the market will have a little more trust in the moat of Meta’s online real estate empire. It will be a way more “established” company with a much longer track record of free cash flow and shareholder value generation.

Note that even for this base case scenario I still assume that Zuckerberg keeps investing heavily in the metaverse for the next 10 years without success. However, I asssume he will give up by the end of the period. At the same time, I keep expecting the same 2.5% effective buyback rate per year as in the bear case scenario, reducing the share count in 2032 to 77.6% of today’s share count.

I still assume the current 50% operating margins by 2032. This may turn out a conservative assumption for the base case, which effectively assumes zero operating leverage, despite a more than 3x revenue increase.

With 50% operating margin, Meta’s family of apps segment would achieve $192.5 billion in operating income in 2032, or roughly $154 billion in earnings after taxes assuming a 20% effective tax rate. At a terminal P/E ratio of 25, Meta’s market capitalization in 2032 would be $3,850 billion - a 8.53x relative to today’s market cap of $451 billion. However, this neglects the impact of the share buybacks. On a per share basis, this scenario would lead to a 11x (8.53x / 0.776), or a CAGR of 27%.

Optionality

This may be deserving of a separate write-up, but I believe Zuckerberg is absolutely right to go all in on the Metaverse. The opportunity is compelling, especially from Meta’s perspective. Meta has the leadership and the resources to pull this off. At the same time, we don`t know if it will work. Given the vast free cash flow that Meta generates, I think the split of free cash flow into buybacks and metaverse investments is ideal for the mid term. In 5 to 10 years, we will have to evaluate the situation.

Reality labs already generated $2.3 billion in revenues in 2021. At scale, it could be a software / hardware business with Apple-like operating margins. More importantly, the metaverse would provide an endless opportunity to expand Meta’s online real estate empire. For now, I could live very well with a 11x over 10 years, even if the metaverse investments turn out to be a total disaster.

Another optionality for Meta comes from financial engineering. A few years ago Apple has pulled off a leveraged buyback by taking on huge loans at low interest rates, and using the proceeds to buy back shares. This has led to a massive jump in earnings per share without any operational improvements in the business.

Meta has the debt capacity to pull of the same move as Apple: it is debt-free, while producing significant free cash flow. Any modest added leverage is effectively risk free, which should result in the corresponding very low interest rates on that debt.

Interestingly, Meta has recently changed its CFO and has just issued $10 billion in bonds at very low interest rates, despite the current macro condition. To move the needle, I would support a leveraged buyback of rather $100 billion, especially if/when interest rates come down a bit further. I believe the leveraged buyback path is rather likely than not at this point. Importantly, it would create significant additional shareholder value on top of the shareholder value creation outlined in my base case scenario.

Disclosure: I own Meta shares