HelloFresh: Leading Subscription Business Primed for Growth after Expectations Reset

HelloFresh: Leading Subscription Business Primed for Growth after Expectations Reset

A short-term bounce, a near term upside surprise and a long-term 10x?

Summary

Best-in-class online food solutions operator trading at 2.3x EV / Adj EBITDA

Meal kit vertical is a cash cow in transition about to return to sustainable growth

Ready-to-eat, growing 50% in 2024, to become the dominant vertical long term

Disclaimer: This writeup is not investment advice and should not be construed as such. I am sharing my research insights and positioning on individual companies for informational and entertainment purposes. In particular, I do not take into account any readers personal financial situation. Please do your own research.

1) Overview

HelloFresh is a leading food solutions company, with a subscription based business model. HelloFresh’s range of offerings span from meal kits for home cooking to ready-to-eat (RTE) meals and even branching into pet food and even quality meat.

Meal Kits (~80% of 2023 revenue): This is HelloFresh's core business model. Customers subscribe to receive weekly deliveries of pre-portioned ingredients, accompanied by chef-curated recipes, making home-cooked meals both accessible and convenient. This model alleviates the burden of meal planning and grocery shopping, fitting perfectly into the bustling lifestyles of modern consumers. Beyond the flagship HelloFresh brand, the company's "Home Cooking" vertical boasts a spectrum of brands such as Green Chef, which specializes in organic and healthy eating options, or EveryPlate, focusing on affordability.

Ready-to-Eat (RTE) Meals (18.4% of 2023 revenue): HelloFresh also provides prepared meals that require minimal or no preparation before consumption, targeting consumers looking for convenience without the need for cooking.

Expansion to Other Verticals: As indicated by the "Pet/Others" category, HelloFresh Group is diversifying its offerings to include solutions for pet food and possibly other related areas, which could include snacks, beverages, or different dietary needs like vegan or gluten-free options.

In essence, HelloFresh's business model is about offering convenient, varied, and quality food solutions directly to consumers, supported by a strong infrastructure and data-driven insights. The D2C model allows HelloFresh to manage the entire customer experience from order to delivery, which can enhance customer satisfaction and loyalty. It also enables them to collect a significant amount of customer data on taste preferences, which can be used to tailor offerings and improve the service. With multiple brands under its umbrella, HelloFresh can streamline operations and leverage shared resources such as marketing, supply chain management, and technology platforms.

2) The Meal Kit Business - An Industry-Leading Cash Cow

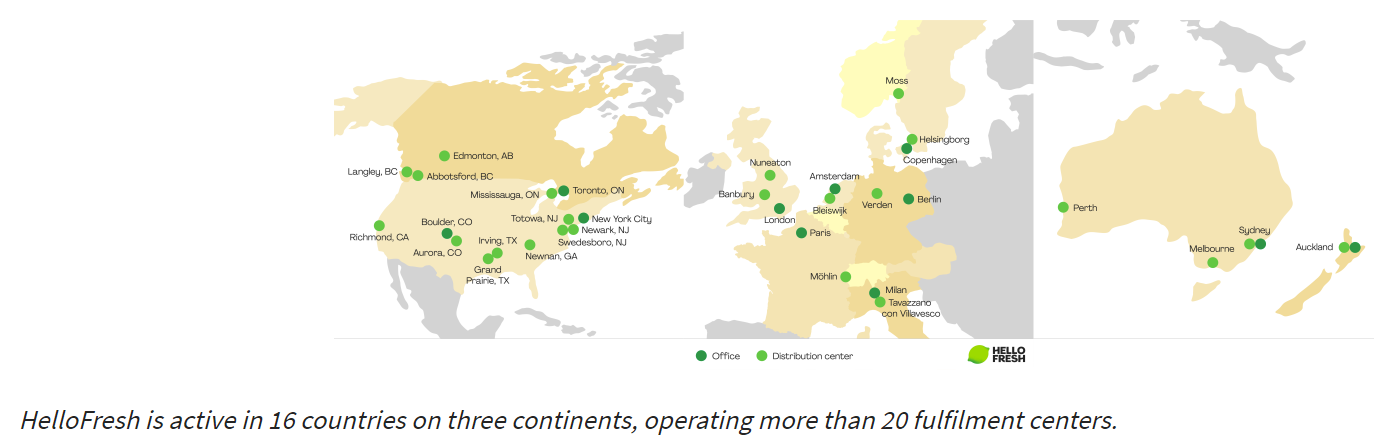

HelloFresh is the clear category leader in the meal kit sector in every single of the 16 countries where it operates in:

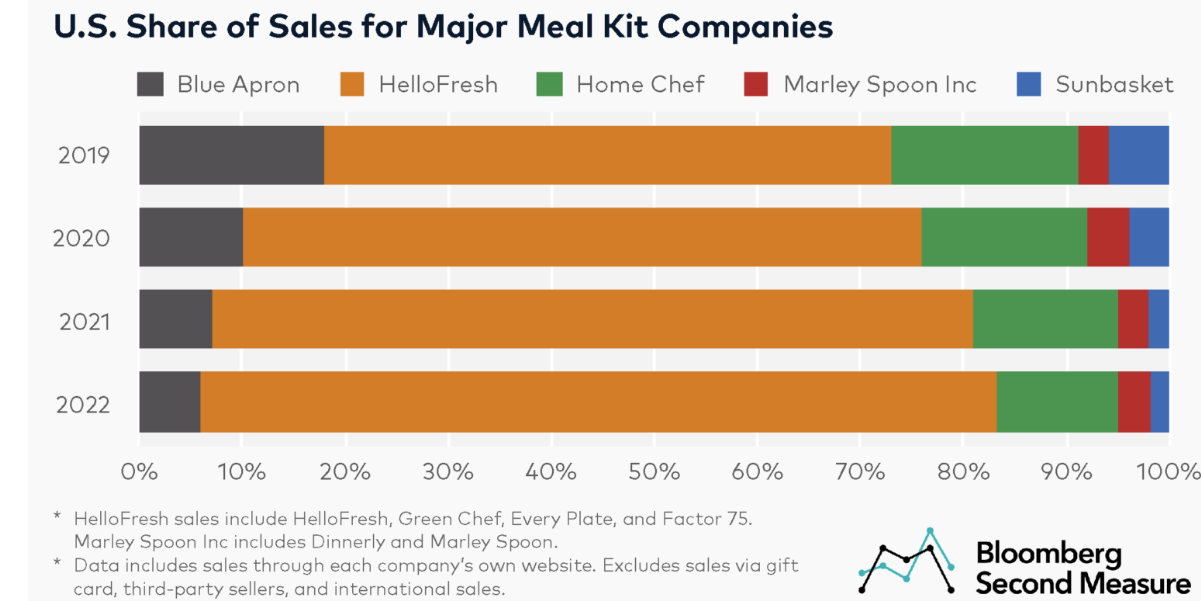

The graphic below from bloomberg secondmeasure demonstrates how HelloFresh took the US market by storm.

HelloFresh is not only larger than its competitors, but also more profitable. In mature markets, HelloFresh operates at adjusted EBITDA margins between 12-15%. In contrast, US competitor Blue Apron was on a path toward bankruptcy, until it was bought out by Restaurant company Wonder Group. In my view, HelloFresh’s total dominance of the meal kit sector is a very strong indicator for operational excellence, which is a key reason to invest for me.

The Meal Kit Business will be at a cyclical low in 2024

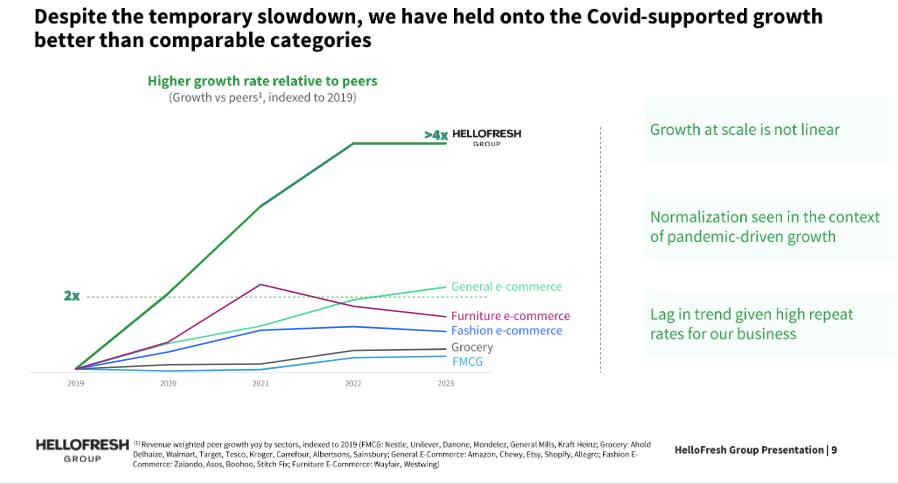

The pandemic was a blessing for HelloFresh, as it allowed the company to increase topline revenues by more than 4x in only four years, far surpassing other e-commerce sectors. Moreover, this growth was incredibly profitable, as HelloFresh could operate at maximum capacities and did not have to invest in marketing. Nevertheless, the growth and profitability of the pandemic period were also artificially high and are now hitting HelloFresh in the form of tough year over year comps. Moreover, the economic environment with high inflation and weak economic growth is an additional challenge. I understand HelloFresh’s meal kits as a lifestyle-upgrade. It will generally be a tougher sell to upgrade people’s lifestyles when the consumer is generally rather squeezed and looks to save. In light of these challenges, it is actually remarkable how well HelloFresh has managed to defend meal kit revenues, as it has to replace churning customers from the pandemic years with new ones during a challenging phase.

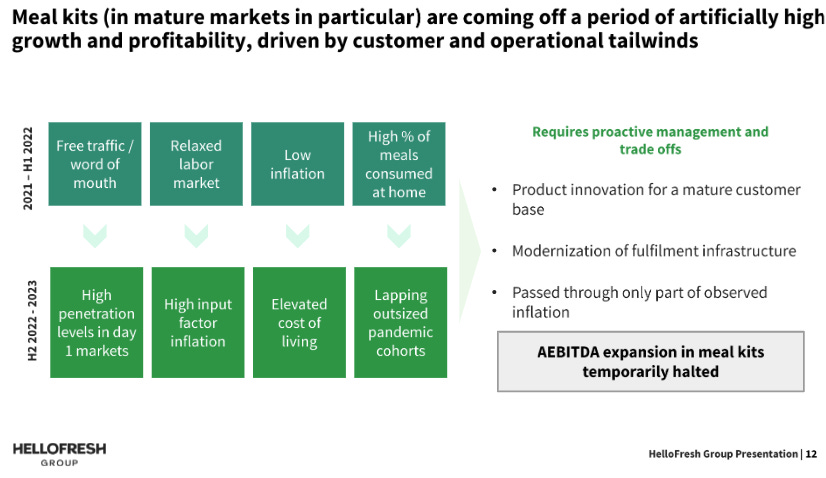

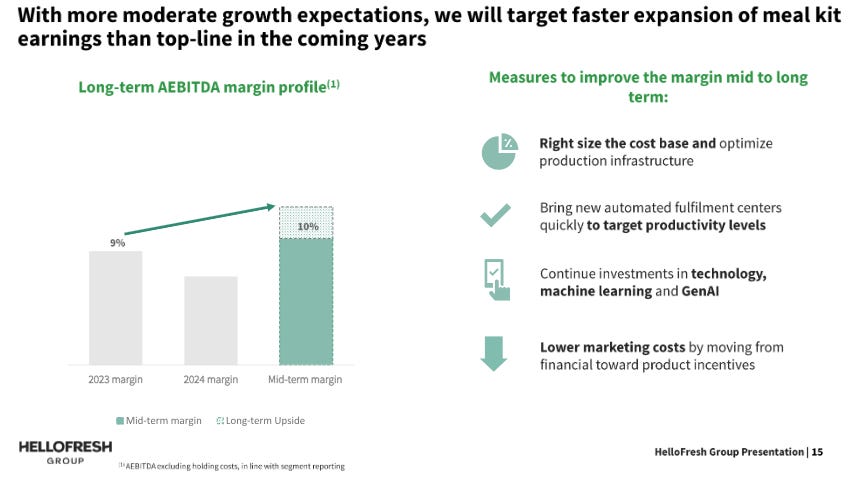

HelloFresh management describes 2023 and 2024 as a consolidation phase for the meal kit business. For 2024, HelloFresh guides for -5% revenue growth in the meal kit business, after revenues were already down in 2023.

On the positive side, HelloFresh indicated in the recent investor call that revenue growth will stabilize in the next quarters. Longer term, management anticipates to return to “sustainable” growth in the meal kit segment. Near term, HelloFresh is suffering from negative operating leverage. Moreover, the company is finalizing their modern fulfilment centers and will operate the existing ones simultaneously until 2025. I anticipate that from 2026 on, EBITDA margins will return to 10% for the meal kit business and stabilize at 12% long term.

Financials of the Meal Kit Segment

For 2026 I am modelling a revenue of €6,131m for the meal kit segment at 10% AEBITDA margins. This would result in adjusted EBITDA of €613m by 2026. Thereafter, I anticipate moderate revenue growth of 2% per year and steady margin expansion to 12%, leading to €812 adjusted EBITDA by 2033. By comparison, the entire enterprise value today is €878m.

Note that the above is my base case scenario. There is substantial upside to these numbers if the new fulfilment centers can bring cost efficiencies that HelloFresh passes on to consumers, increasing affordability. Moreover, the economic environment will likely substantially improve from today, which could strongly increase the customer acquisition. HelloFresh is also constantly optimizing its customer retention strategies (e.g. lifelong snacks as long as the subscription is active). I believe it is save to say that HelloFresh’s customer acquisition and retention strategies will only get better over time, not worse.

3) Ready-to-Eat: The Rising Star About to Become More Important than Meal Kits

In the perception of many investors, HelloFresh seem to be nothing more than a cooking box provider without a moat. Supermarkets have tried to provide cooking boxes - without success. Competitors tried to go after HelloFresh - without success. After all, the core meal kit business is a profitable subscription business thanks to operational excellence in comparison to the competitors. Still, I would probably not invest in HelloFresh for the long term if they only had this cash cow. The evidence suggests that HelloFresh is more than that, a platform business to be precise.

In November 2020, flush with cash from its meal kit business, HelloFresh acquired Factor 75, a Chicago-based meal kit startup, for $177 million. At the time, Factor was described as “…a provider of fully-prepared, fresh meals that combine health, convenience and restaurant-quality taste.”

Within just three years, HelloFresh scaled Factor 75’s revenues 10x to €1,400m in 2023. For 2024, HelloFresh guides for another 50% revenue growth, bringing revenues to €2,100m, or 26% of HelloFresh’s 2024 revenues.

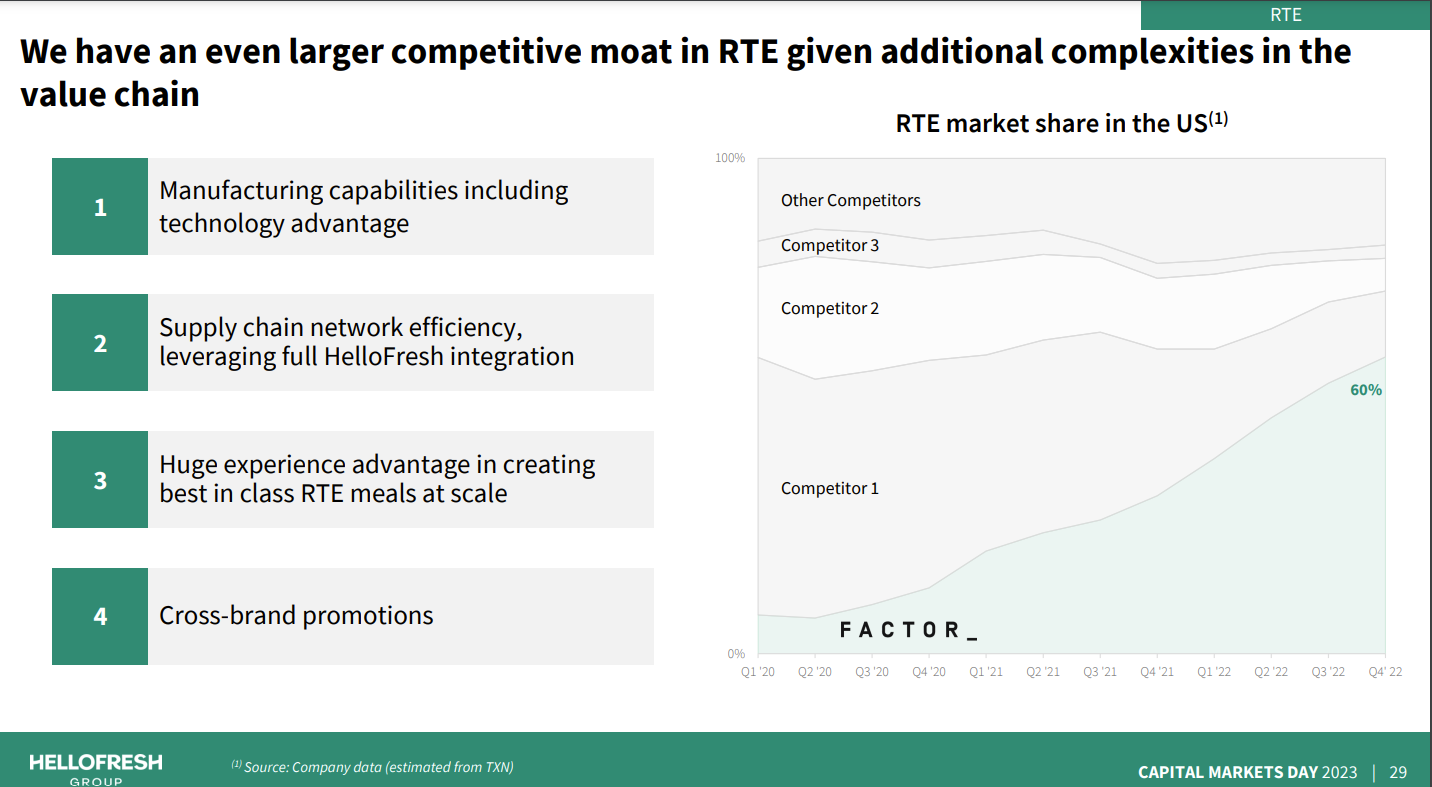

In the process, HelloFresh, once again, ate the competition alive, by achieving a 60% market share in the US already by the end of 2022:

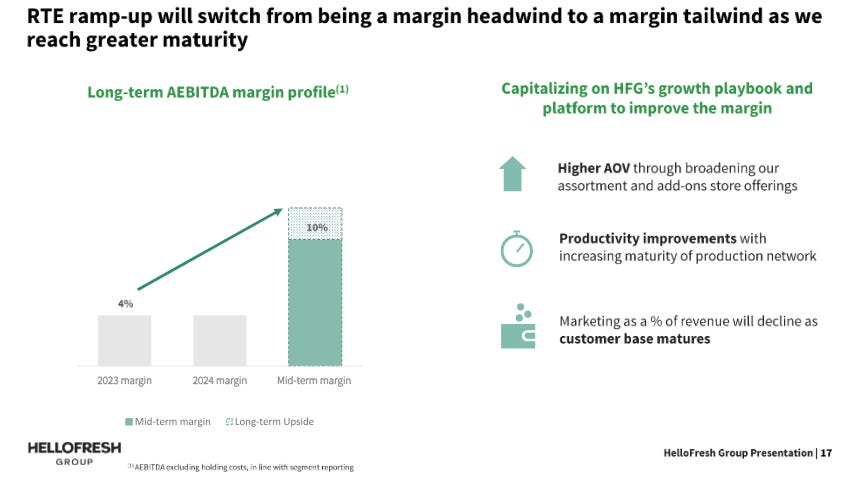

Such a success story would have been impossible without leveraging the technology and supply chain platform of HelloFresh’s existing business. Despite the growth, Factor 75 already operates at 4% EBITDA margins. Over the long term, management guides for the RTE segment to achieve the same EBITDA margins north of 10% as for the meal kit business.

As management guides for 50% growth towards €2.1b revenues in 2024, while the internationalization of Factor 75 is only beginning, the evidence suggests that the ready-to-eat segment has a significantly larger addressable market than the meal kit business.

Does Factor have a Moat?

Factor distinguishes itself from on-demand delivery services like UberEats by offering a subscription-based model focused on delivering healthy, chef-prepared meals directly to consumers. This model does have several competitive strengths:

Centralized Production: Factor uses centralized kitchens to prepare meals, allowing for consistency in quality and taste. Centralized production can create economies of scale, reduce costs per unit, and maintain control over the culinary process and ingredient sourcing.

Reduced Logistics Complexity (and Costs): By sending a weekly package of meals all at once, Factor simplifies the logistics of delivery compared to on-demand services that must manage complex logistics with multiple restaurant partners and deliveries.

Subscription Model: The subscription model provides a predictable revenue stream and can build a more loyal customer base. Subscribers are more likely to provide a steady flow of income, whereas on-demand services are more transactional and can be more susceptible to customer churn.

Health and Wellness Focus: Factor targets health-conscious consumers looking for convenience without compromising on dietary preferences or goals. This focus on health and nutrition creates a niche market that may be underserved by broader on-demand food delivery services.

Prepared Meal Convenience: Factor specializes in delivering meals that are already cooked and only require reheating, which is different from most on-demand services that deliver food that is intended to be consumed immediately after arrival. The convenience of having a week's worth of meals prepared in advance can cater to busy individuals who might not have the time to cook daily or prefer not to order from restaurants frequently due to health, dietary restrictions, or cost considerations.

The careful reader will notice how all these strengths directly leverage HelloFresh’s existing supply chain platform from the meal kit business. Moreover, HelloFresh can leverage the existing technology. For example the app is exactly the same as for the meal kits. Even the customer acquisition strategies will not be materially different from meal kits, so HelloFresh has a massive advantage over any would-be competitor that has to figure out and scale all these issues from the scratch (while burning more money than HelloFresh’s Factor and while not having a meal kit cash cow.

Below is a screenshot from the current Factor website. HelloFresh users will immediately recognize the brand design. The ready to eat food pictured hints at a low carb, high protein choice that is not even an option at HelloFresh yet. Note also how Factor cleverly hints at loyalty benefits. Personally, I can’t wait to try the service in Europe.

Impressively, Factor already offers a choice between 35(!) meals per week. GOOD LUCK to anyone trying to compete with Factor. Frankly, I don’t see why any competitor would be more successful competing with HelloFresh in RTE than in mealkits. The way Factor destroyed the competition in the US is more than just a hint.

Financials of the Ready-to-Eat Segment

HelloFresh guided for 50% revenue growth in 2024, or €2.1b in revenues at the same EBTIDA margin of 4% as in 2023. Moreover, management mentioned that 2023 growth was capacity constrained, which hints at the growth runway. And it is intuitive that RTE will be way bigger than meal kits, as customers no longer have to cook.

I am modeling 35% and 30% revenue growth in 2025 and 2026, resulting in 2026 revenue of €3,686. At HelloFresh’s mid term EBITDA margin target of 10%, that would be already €369m in EBITDA.

For the next 9 years following 2024, I am modelling a revenue CAGR of 17.3%, resulting in RTE segment revenues of €8.8b. At a 12% AEBITDA margin, this would result in AEBITDA of €1,056m by 2033.

In my base case model I anticipate RTE revenues will surpass meal kit revenues by 2029 and RTE AEBITDA will surpass meal kit EBITDA by 2030.

4) New Business Lines

As they should be for a proper platform business model, HelloFresh is seeking to identify the next billion dollar business lines. The Pets Table and Good Chop represent HelloFresh's strategic expansion into new market segments using their established direct-to-consumer platform.

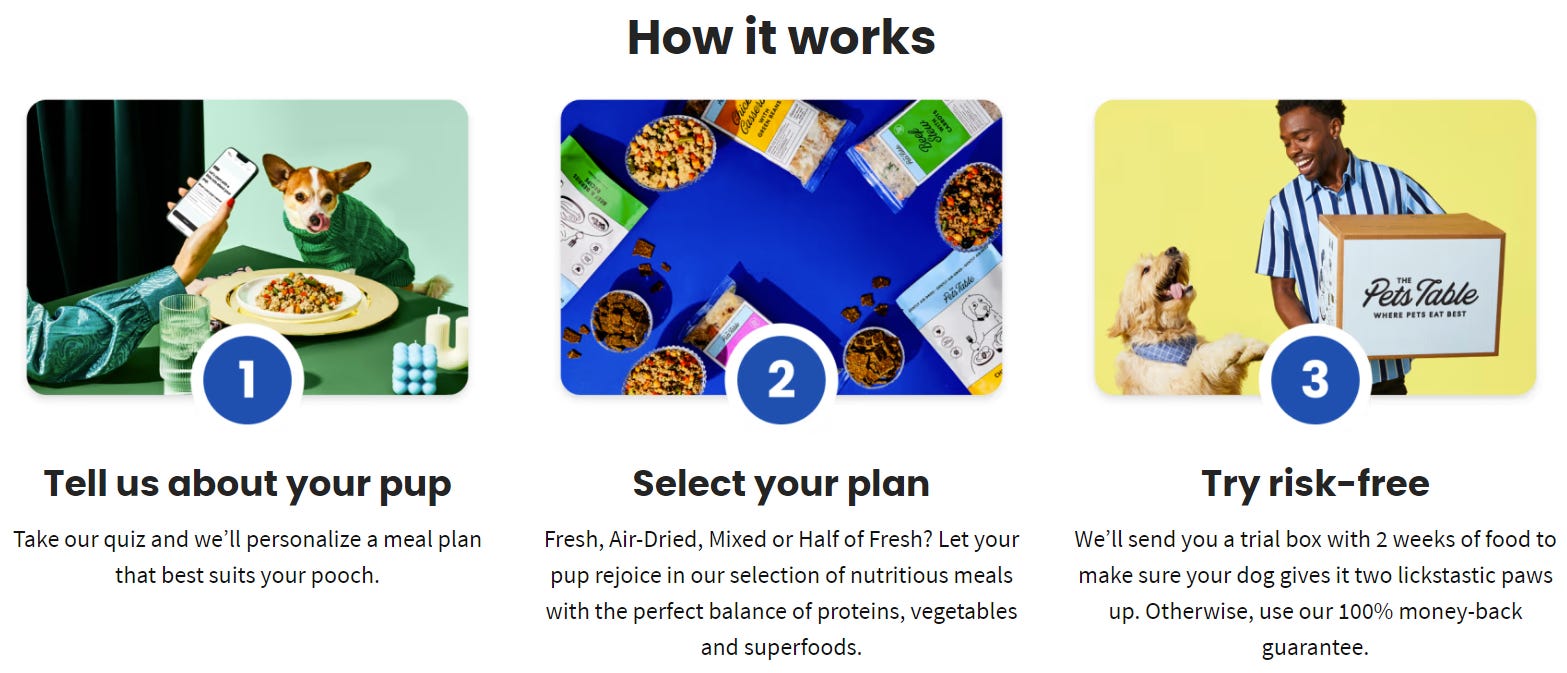

The Pets Table is a premium pet food brand developed by HelloFresh, reflecting the company’s expansion into the high-potential pet food market. Recognizing the deepening bond between pet owners and their pets, particularly following the pandemic, The Pets Table aims to deliver healthy and convenient solutions tailored to pets' nutritional needs. The brand focuses on providing pets with a wholesome, minimally-processed diet, collaborating with veterinarians to develop recipes that meet the standards set by the Association of American Feed Control Officials (AAFCO) for all life stages of dogs.

The Pets Table offers several plans, including Fresh, Air-Dried, Mixed, and Half of Fresh, designed to fit various budgets and cater to different preferences. For example, their Fresh plan includes human-grade dog food made without preservatives or fillers and is delivered frozen, while the Air-Dried plan provides a healthy and shelf-stable alternative to kibble. Personalization is also a key aspect of their service, with meal plans customized to meet each pet's unique caloric needs based on information provided by the pet owner through a quiz.

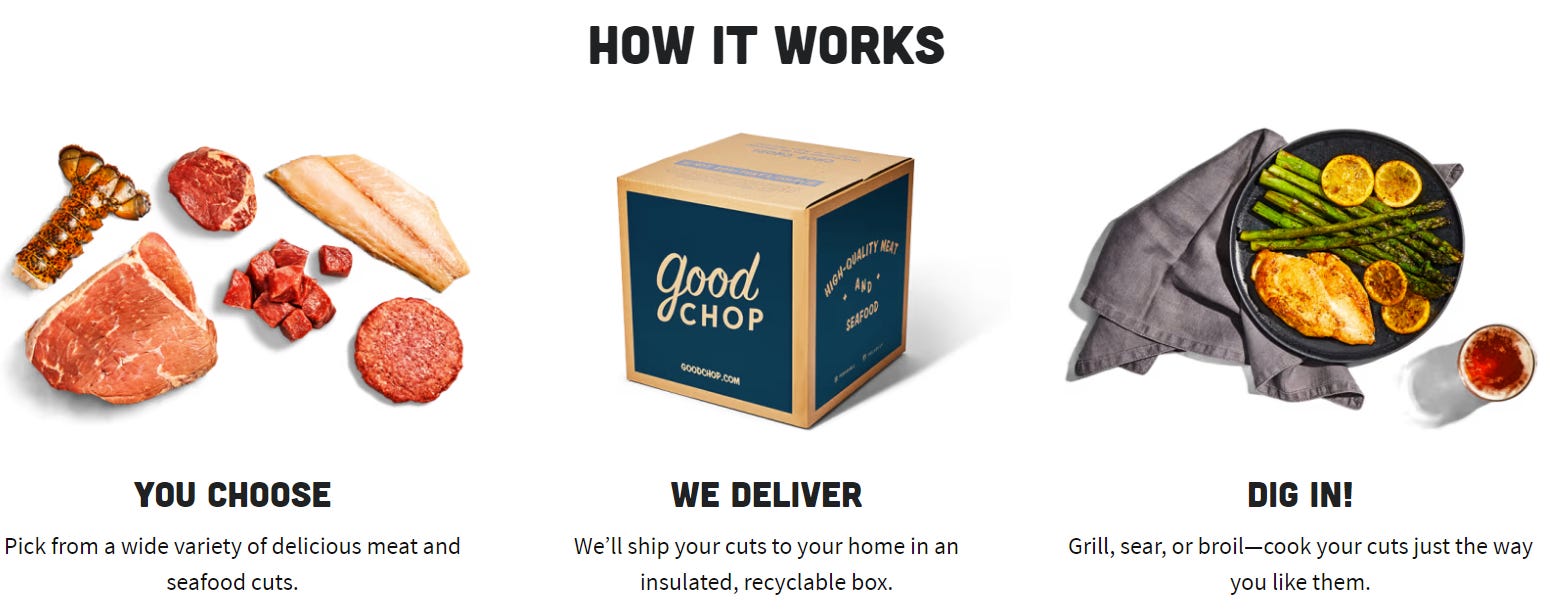

Good Chop is HelloFresh’s American meat and seafood delivery service. They focus on high-quality, sustainably sourced, and responsibly raised products with no antibiotics or added hormones. Their offerings include a variety of meats and seafood that are all from the U.S., emphasizing quality and flavor. Customers can choose their preferred cuts, and Good Chop delivers them in customizable, insulated boxes with flexible delivery options, accommodating those who prioritize premium, ethically sourced meat and seafood in their cooking.

At the 2023 capital markets day, HelloFresh indicated that revenue share for these two lines was still below 1%. I believe there is a lot of room for HelloFresh to experiment. With quality meat, they chose a segment that is not currently well served by supermarkets (that may also provide home delivery). As a dog owner, I can confirm that online ordering of quality food has a lot of potential and is a very fragmented market. It is not hard to see HelloFresh having stellar success as with Factor in any of these new businesses over the long term.

Through these new lines, HelloFresh leverages its existing supply chain, technology, and direct-to-consumer expertise, similar to the way antenna systems like AMT can service multiple clients. This allows HelloFresh to efficiently scale its operations and potentially increase the average revenue per user by cross-selling different types of products within its customer base.

An Analogy - American Tower Corp

Many years ago I came across American Tower Corp. AMT leases leases antenna space on multi-tenant communication towers to wireless and broadcast companies. The company is one of the great long term compounders. The secret sauce - as I understand it - is their ability to add more antennas (for new clients) to existing towers without significant additional investment. Unfortunately I never invested, but I never forgot about this amazing catch of being able to generate more revenues at little extra cost from the existing infrastructure.

Drawing a parallel, HelloFresh similarly similarly capitalizes on its established distribution network to expand its product offerings, as evidenced by the stellar success with Factor. Likewise, Good Chop and The Pets Table, can creating a recurring revenue model that grows with every additional customer or product line added. HelloFresh can cross sell to its existing and former client database. They key advantage would be to sell more and more through the same weekly package delivery. A true advantage of the weekly subscription model over the on demand deliveries by uber or supermarkets.

At least to me, these are the early indications of a potentially really great business model in the long run. While HelloFresh only guides for 5% revenue growth in 2024, the long term growth runway is basically unlimited if the company plays its cards well and the execution so far is very promising.

5) Valuation

As explained above, I am modelling €802m adjusted EBITDA by 2026 and €1683 adjusted EBITDA by 2033.

Of course adjusted EBITDA is not free cash flow, but it is a good starting point. For 2023, the following factors should be considered. Please note these are just estimates as the company has not yet revealed the FY 2023 results at the time of this writeup:

In line with HelloFresh’s segment reporting, the AEBITDA margins are before the application of Holdco / headquarter costs. For 2023, Holdco costs should be about €160-170m, and I am modeling a gradual increase to €260m by 2033.

Stock based compensation is about €100m in 2023 and I am modeling a gradual increase to €180m by 2033.

IFRS lease accounting, regrettably, removes rent payments from the EBITDA calculation. In turn, I deduct lease costs (lease plus interest on the lease) of about €100m in 2023 and model a gradual increase to €180m by 2033 as HelloFresh builds out the infrastructure.

Capex are expected to fall to €250m by 2025 according to the 2023 Capital Markets Day presentation. I am modelling a gradual increase to €330m by 2033.

Taxes are calculated assuming a 30% tax rate on AEBITDA - Holdco - SBC - Lease Cost - Capex (assumption is capex are about in line with depreciation).

The table below shows the resulting assumptions of my current base case, given the current information. Please make sure to recognize the substantial uncertainty surrounding these numbers and adjust as you see fit.

I am arriving at a free cash flow (no SBC deducted) of €335m by 2026 and €925m by 2033. As you can see, I am not anticipating substantial negative free cash flow for 2024 and I anticipate HelloFresh to become free cash flow positive from 2025. In total, the free cash flow for the next 10 years would accumulate to €4,748m: About 4x today’s market cap.

I deduct SBC from FCF to arrive at my definition of owner earnings for HelloFresh. Based on these assumptions, HelloFresh currently trades for about 5.2x owner earnings in 2026. Assuming my assumptions prove correct and HelloFresh has substantial growth runway beyond 2033, a multiple of 20x owner earnings does not seem unreasonable. In that scenario, HelloFresh’s share market cap would be about 11x higher by then.

My cumulative free cash flow for the next 10ys is about 3x higher than the cumulative SBC. HelloFresh should those have significant room to buy back more shares or pay a dividend, not even accounting for the current net cash of about €300m. I hope the company will aggressively buy back shares after the recent crash. Alternatively, the company can push for more aggressive growth or even acquisitions, especially once consumer sentiment inevitably improves from the current squeeze.

6) Did Mr. Market Overreact?

HelloFresh’s share price reaction following the preliminary numbers on March 7 was truly one of a kind. HelloFresh revealed 2023 numbers perfectly in line with prior guidance. However, for 2024 it guided for AEBITDA of €375m at the midpoint, apparently about 1/3 below broker assumptions. Moreover, HelloFresh pulled it ambition to achieve 2025 revenue of €10b and €1b AEBITDA as “unrealistic” given the environment.

Frankly, I did not expect anyone was still hoping for these 2025 numbers to realize. HelloFresh’s share price peaked at €34 in mid September 2023. Since then numbers were disappointing and especially 2023 guidance had been cut substantially in November, as a result of which the share price already dropped about 2/3s to €11 before the new numbers.

Sensing an overreaction to bad news by Mr Market, I placed an order on Friday morning at €8,00 which did not get filled for 15 minutes as the share price crashed. I later updated my order at €7,00 and with a 15 minute delay it got filled. I have never experienced placing a buy order substantially above the recent transaction price and not getting filled. It is hard for me to make sense of that. I suspect there was a substantial selling pressure with little buy orders so market makers struggled heavily.

Eventually the share price bottomed at €6,30 (I was luckily on the buy side of that transaction). Down almost 50% from the prior day(!!). In light of the fundamentals I present in this writeup and considering that HelloFresh’s share price already dropped 2/3s from last summer when things looked more rosy, I would characterize this reaction as an outright nervous breakdown by Mr. Market. Without doubt, there were big sellers wanting to go out at almost any price and immediately so.

In defense of Mr. Market, I was also negatively surprised by the EBITDA guidance for 2024. While the growth guidance came in as I expected and I also expected them to pull the 2025 “ambition” (though not necessarily at this point). Now, if longs absolutely did not see all of that coming (despite the drop in share price and the guidance cut from November), then yes, that warrants a substantial fall in share price.

It is important to consider that HelloFresh is a heavily shorted stock. Hedge Funds have access to credit card data, at least in the US. So they can proxy for HelloFresh’s US sales almost in real time. I believe Hedge Funds were waiting for this negative surprise to happen, anticipating a selloff (I am unfortunately not that smart or have the credit card data and thus had a pretty substantial HelloFresh position before Friday). IMO next week these hedge funds should cover. I estimate the chances that HelloFresh goes bankrupt short or near term a straight zero. The selloff was more than hedge funds could have reasonably expected. So I think hedge funds will cover next week.

As it relates to the longs that got hit by surprise and panic-sold their shares. I think they are done. The weak hands without a long term conviction should be out now.

I believe this is a very beautiful setup for a short term bounce in the next week.

Long term, it is up to HelloFresh to deliver. And there is an important angle of view. HelloFresh did disappoint investors with guidance they could not achieve. They have clearly acknowledged and explained the mistakes in the call on Friday. Now it is natural for investors to extrapolate recent events, losing not only trust in management, but also anticipating that they will keep missing their targets.

I am happy to take the other view on that angle. Thursday’s guidance was a total reset. I believe the HelloFresh Management team was tired of not being able to meet old and overambitious targets and keep walking and be pressured behind them. IMO chances are that HelloFresh took the opportunity of this reset in expectations to do what all smart management teams do: Under promise and overdeliver.

In sum, I believe HelloFresh has it all. Chances for a short term bounce are good. Chances for a mid term positive surprise are also good if management learnt the right lesson. And most importantly, despite the temporary hiccups in a challenging macro environment. The long term potential is massive and HelloFresh has what it takes to live up to it.

Thanks. Assuming they achieve guidance, current valuation looks definitely attractive. I am a bit hesitant about the general economics of the industry though… Low contribution margins, high marketing spend needed, heavy logistics... and the G&A looks heavy in absolute terms (albeit not as a % of revenue). I would think it would be easy for management to cut cost to achieve healthy margins with their 8bn topline. Anyhow great write up as usual!

Thanks, how can they possibly hit their AEBITDA guidance of EUR 350-400mn for FY24, with only EUR 17mn of AEBITDA in Q1 24? Any thoughts would be appreciated!